Table of Contents

Introduction: Understanding the Global Economy as a Business Essential

The Global Economy is the vast, interconnected system through which countries, businesses, governments, financial institutions, and individuals exchange goods, services, capital, technology, knowledge, and human talent. It is not a distant concept reserved for economists or policymakers. It is the operating environment in which every modern business, entrepreneur, and workforce participant exists. No country, no company, and no individual is fully insulated from its movements, pressures, and opportunities.

Understanding the Global Economy is a business essential because it directly shapes business success, economic growth, investment decisions, employment conditions, living standards, and the long-term progress of the world’s population. When the Global Economy expands, businesses find new markets, investors gain confidence, and workers benefit from rising wages. When it contracts, supply chains break, revenues fall, and governments scramble to respond. The interconnectedness of modern economic activity means that a disruption in one region rapidly transmits across others.

Business leaders, entrepreneurs, investors, policymakers, researchers, students, and professionals who understand the Global Economy are better equipped to interpret trends, anticipate risks, and identify opportunities before they become obvious to the rest of the market. This understanding is not optional. It is a competitive advantage in a world where decisions made in Washington, Brussels, Beijing, or Nairobi can affect businesses operating thousands of miles away.

What makes the Global Economy particularly fascinating is that it does not move for a single reason. It is driven by eight interconnected forces that continuously influence one another: global trade, global finance, global production, global innovation, the global workforce, global resources, global economic governance, and the sustainable economy. Together, these forces shape how wealth is created, distributed, and sustained across the world.

Think of the Global Economy less as a machine with fixed parts and more as a living ecosystem, where every element interacts with every other element. A shift in trade policy affects finance. A disruption in production affects innovation timelines. Understanding these relationships is what separates reactive decision-making from strategic foresight.

This article explores all eight forces in depth, building a comprehensive picture of how the Global Economy functions, why it matters, and what businesses, governments, and individuals can do to navigate it more effectively.

Table 1: Eight Forces Driving the Global Economy

| Force | Contribution to the Global Economy |

| Global Trade | Connects markets, enables specialization, and expands economic opportunity across borders |

| Global Finance | Channels capital to productive uses and sustains investment, credit, and financial stability |

| Global Production | Distributes manufacturing and value creation across countries through integrated supply chains |

| Global Innovation | Drives productivity growth, creates new industries, and strengthens long-term competitiveness |

| Global Workforce | Supplies skills, creativity, and leadership that fuel economic growth and business performance |

| Global Resources | Provides the natural foundation for industrial production, energy, agriculture, and infrastructure |

| Global Economic Governance | Establishes rules, institutions, and policies that enable the world economy to function efficiently |

| Sustainable Economy | Integrates environmental responsibility into growth strategies for long-term resilience |

1. Global Economy Through Global Trade

Global trade is one of the foundational pillars of the Global Economy. It is the mechanism through which countries exchange goods and services based on specialization, comparative advantage, and market demand. When countries focus on producing what they do most efficiently and trade for what others produce better, the overall output of the world economy expands. This principle, first articulated by economist David Ricardo in the nineteenth century, remains as relevant today as when it was written.

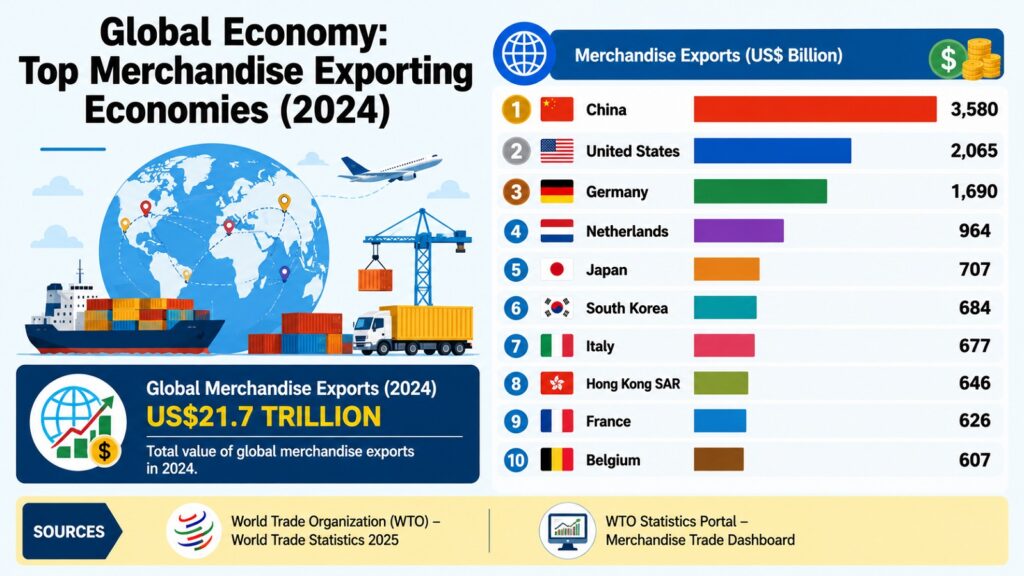

Beyond the theory, Global Trade has delivered measurable transformation. The World Trade Organization estimates that global merchandise trade volumes grew more than forty-fold between 1950 and 2020. Economies that actively participated in international trade, particularly across East and Southeast Asia, achieved productivity improvements, income growth, and poverty reduction at speeds that would have been unimaginable through domestic production alone. South Korea, for instance, built one of the world’s most competitive manufacturing and technology export sectors within a single generation by integrating deeply into global trade networks.

Trade does more than move goods across borders. It transfers technology, spreads best practices, increases competitive pressure on domestic producers, and forces efficiency improvements that raise productivity economy-wide. When a domestic manufacturer must compete with imported goods, it either improves its operations or exits the market. Those that survive are leaner, more innovative, and more competitive globally.

For businesses, international trade creates access to larger markets, more diverse customer bases, and lower-cost inputs. A company that sources materials from multiple countries, manufactures in the most efficient location, and sells to customers in dozens of markets is more resilient than one confined to a single domestic economy. This is not merely a feature of multinational corporations. Small and medium enterprises that access global supply chains or export to international markets often outperform domestically focused peers.

Looking ahead, global trade faces evolving pressures. Rising geopolitical tensions, supply chain vulnerabilities exposed during the COVID-19 pandemic, and shifting trade agreements are pushing businesses and governments to reassess supply chain geography. The movement toward near-shoring, friend-shoring, and diversification of sourcing reflects a recognition that efficiency and resilience must be balanced. Trade will continue to be a defining force of the Global Economy, but its architecture is likely to evolve significantly over the coming decade.

Table 2: Eight Key Principles of Global Trade in the Global Economy

| Principle / Component | Contribution to the Global Economy |

| Comparative Advantage | Enables countries to specialize and trade for mutual economic gain |

| Export-Led Growth | Drives GDP expansion through access to larger international markets |

| Trade Agreements | Reduce tariffs and barriers, increasing market access and business opportunities |

| Technology Transfer | Spreads innovation and productivity improvements across trading partners |

| Supply Chain Integration | Connects producers across countries into efficient global value networks |

| Import Competition | Forces domestic firms to improve efficiency and remain competitive |

| Foreign Exchange Markets | Facilitate currency conversion required for international trade settlement |

| Trade Diversification | Reduces economic dependence on single markets, improving national resilience |

2. Global Economy Through Global Finance

Global finance is the circulatory system of the Global Economy. Without efficient financial systems, capital cannot reach the businesses, governments, and projects that need it most. Global finance encompasses banking institutions, capital markets, foreign direct investment, international lending, payment systems, currency exchange mechanisms, and the regulatory frameworks that govern them.

Financial systems do far more than process transactions. They allocate scarce capital toward its most productive uses, transforming savings into investment and investment into economic growth. When financial systems function well, entrepreneurs can access credit, businesses can expand internationally, governments can fund infrastructure, and investors can deploy capital across borders with confidence. The International Monetary Fund has consistently documented the strong relationship between financial depth and long-term economic development, particularly in emerging markets where access to finance often determines which businesses survive and which do not.

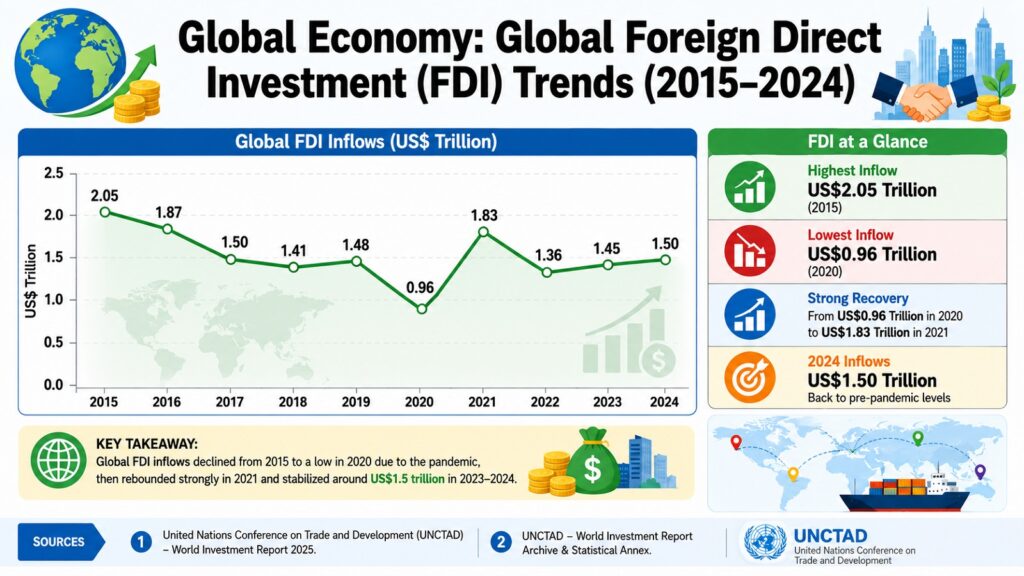

Foreign direct investment is one of the clearest expressions of how global finance strengthens the Global Economy. When a technology firm builds a manufacturing facility in Southeast Asia, or when a private equity fund acquires a business in Eastern Europe, capital crosses borders in ways that create employment, transfer skills, build productive capacity, and generate tax revenue. According to UNCTAD, global foreign direct investment flows totaled approximately 1.3 trillion dollars in 2023, a figure that demonstrates the enormous scale at which cross-border capital continues to move.

The 2008 global financial crisis is perhaps the most instructive modern case study in how financial interconnection can amplify both opportunity and risk. The crisis originated in the United States housing market but spread rapidly through the global banking system, triggering recessions in dozens of countries and exposing the vulnerabilities of poorly regulated financial integration. The response, coordinated through institutions like the G20 and the Financial Stability Board, demonstrated that effective global financial governance can limit contagion when cooperation is genuinely prioritized.

Financial innovation continues to reshape how the Global Economy operates. Digital payment systems, mobile banking, fintech platforms, and decentralized finance are expanding financial access to populations and businesses previously excluded from formal financial systems. These developments have particular significance in emerging economies, where financial inclusion can accelerate entrepreneurship, reduce poverty, and drive sustained economic growth.

Table 3: Eight Strategic Functions of Global Finance in the Global Economy

| Function / Institution | Contribution to the Global Economy |

| International Monetary Fund | Provides financial stability support and policy advice to member countries |

| World Bank Group | Funds development projects and reduces poverty in emerging economies |

| Capital Markets | Enable businesses and governments to raise long-term investment capital |

| Foreign Direct Investment | Transfers capital, technology, and skills across borders, supporting growth |

| Central Banks | Manage monetary policy, inflation, and financial system stability nationally |

| Foreign Exchange Markets | Enable currency conversion supporting international trade and investment |

| Fintech and Digital Payments | Expand financial access and reduce transaction costs globally |

| Basel Regulatory Framework | Sets international banking standards to reduce systemic financial risk |

3. Global Economy Through Global Production

Global production is the engine that transforms inputs into economic value. It encompasses manufacturing, industrial specialization, logistics, transportation, procurement, outsourcing, and the global value chains that link producers across multiple countries into integrated production systems. Production is not simply the act of making things. It is the coordinated creation of value across interconnected geographies, industries, and business relationships.

The rise of global value chains over the past four decades has fundamentally changed how production works. Instead of a single country or company producing everything required for a finished product, production is now distributed across multiple countries, with each contributing the stage of the process where it holds the greatest advantage. An automobile manufactured in Germany may contain electronics from South Korea, steel from Brazil, software components from India, and design work from the United Kingdom. Each stage adds value within a deeply integrated global system.

This distribution of production has delivered substantial economic benefits. Countries that participate in global value chains typically achieve faster productivity growth, greater access to advanced technologies, and higher wages than those that remain outside them. McKinsey Global Institute research has consistently found that participation in global value chains correlates strongly with economic development, particularly for lower-income countries gaining entry into higher-value production stages over time.

For businesses, global production decisions involve balancing cost efficiency, quality control, logistical complexity, and supply chain risk. The COVID-19 pandemic exposed the fragility of highly concentrated supply chains, particularly in sectors like semiconductors, pharmaceuticals, and consumer electronics where production was heavily concentrated in a small number of locations. In response, businesses and governments have moved toward greater supply chain diversification, regional production hubs, and increased inventory buffering to improve resilience.

Looking forward, smart manufacturing technologies, artificial intelligence, robotics, and digital supply chain management are redefining what efficient production looks like. Automation is reducing the labor-cost advantages that drove offshore production decisions for decades, potentially reshaping which countries hold production advantages in the future. Countries investing in advanced manufacturing, engineering talent, and digital infrastructure are building the foundations for long-term production leadership. The businesses and economies that invest in advanced production capabilities today are positioning themselves for competitive advantage in tomorrow’s Global Economy.

Table 4: Eight Components of Global Production in the Global Economy

| Component / Capability | Contribution to the Global Economy |

| Global Value Chains | Distribute production across countries to maximize efficiency and competitiveness |

| Industrial Specialization | Allows countries to focus on high-value-added production stages |

| Logistics and Freight | Connect producers and markets, enabling seamless global trade flows |

| Outsourcing and Offshoring | Reduce production costs and enable businesses to focus on core capabilities |

| Lean Manufacturing | Minimizes waste and improves production efficiency across supply chains |

| Supply Chain Resilience | Reduces vulnerability to disruptions through diversification and redundancy |

| Smart Manufacturing | Uses automation and AI to increase production speed, quality, and flexibility |

| Procurement Strategy | Optimizes sourcing decisions to balance cost, quality, and supply security |

4. Global Economy Through Global Innovation

Innovation is the force that prevents the Global Economy from stagnating. It is the process through which new ideas, technologies, business models, and organizational capabilities are created, refined, and deployed to increase productivity, solve problems, and generate sustainable economic growth. Without innovation, economies would eventually exhaust the gains available from simply doing existing things more efficiently.

The relationship between innovation and economic growth is well established. Nobel Prize-winning economists like Paul Romer have demonstrated that ideas and knowledge are the ultimate drivers of long-run growth, distinct from physical capital and labor because they do not deplete with use. A new manufacturing process or a more efficient logistics algorithm can be applied across an entire economy simultaneously, multiplying its economic impact far beyond the original investment in its development.

Modern innovation operates across multiple dimensions simultaneously. Advances in artificial intelligence are transforming industries from healthcare diagnostics to financial risk modeling. Semiconductor innovation is enabling more powerful computing at lower cost. Biotechnology is reshaping pharmaceutical development. Cloud computing is democratizing access to enterprise-grade technology for businesses of every size. These developments are not independent. They reinforce each other, creating compounding productivity improvements that ripple through the entire Global Economy.

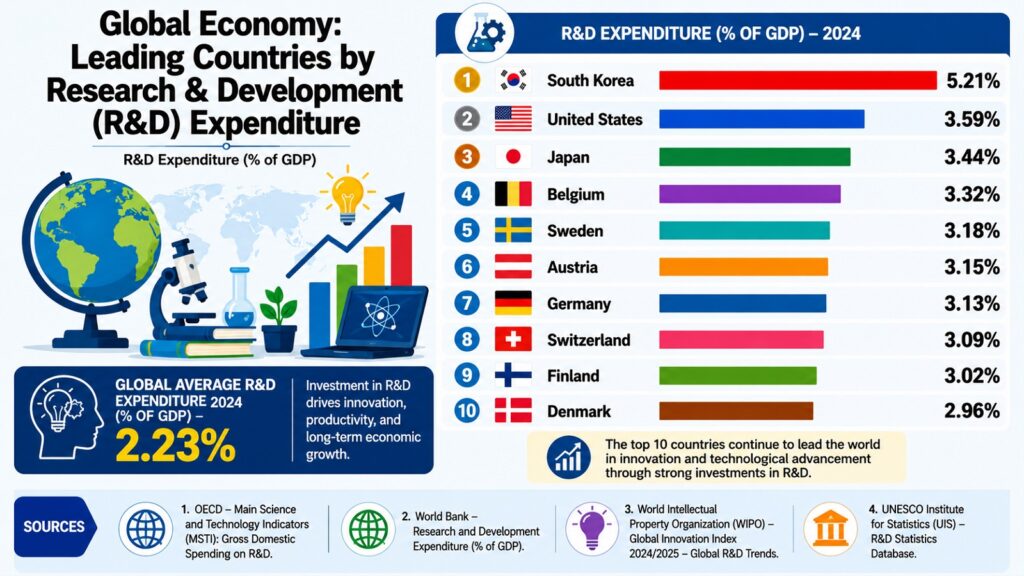

A compelling case study is South Korea’s transition from a low-income agricultural economy in the 1960s to a global leader in semiconductor and consumer electronics innovation within three decades. This transformation was driven by deliberate investment in research and development, engineering education, technology licensing, and close collaboration between government policy and private sector ambition. Samsung and LG emerged from this ecosystem to become global technology leaders, demonstrating that innovation capacity can be deliberately built rather than simply inherited.

Maintaining innovation-driven competitiveness requires organizations to invest continuously in research and development, cultivate talent, create environments that tolerate intelligent risk-taking, and build partnerships across the global innovation ecosystem. Countries that consistently invest in education, research infrastructure, and business-friendly regulatory environments tend to attract the human capital and investment that sustain long-term innovation leadership. The lesson is clear: innovation is not an accident but the result of deliberate, sustained strategic choices that position economies for advantage in the Global Economy.

Table 5: Eight Innovation Drivers Contributing to the Global Economy

| Innovation Driver / Technology | Contribution to the Global Economy |

| Artificial Intelligence | Automates complex tasks, improves decision-making, and drives productivity across sectors |

| Semiconductor Technology | Powers computing advances that underpin virtually every digital industry globally |

| Biotechnology | Accelerates pharmaceutical development, agricultural productivity, and healthcare improvements |

| Cloud Computing | Enables scalable, low-cost technology access for businesses and governments worldwide |

| R&D Investment | Builds the knowledge base from which commercially valuable innovations emerge |

| Digital Transformation | Restructures business models and operations for greater efficiency and market reach |

| Green Technology | Develops clean energy and sustainability solutions that support long-term economic growth |

| Open Innovation Ecosystems | Accelerate knowledge sharing and commercialization across companies and countries |

5. Global Economy Through Global Workforce

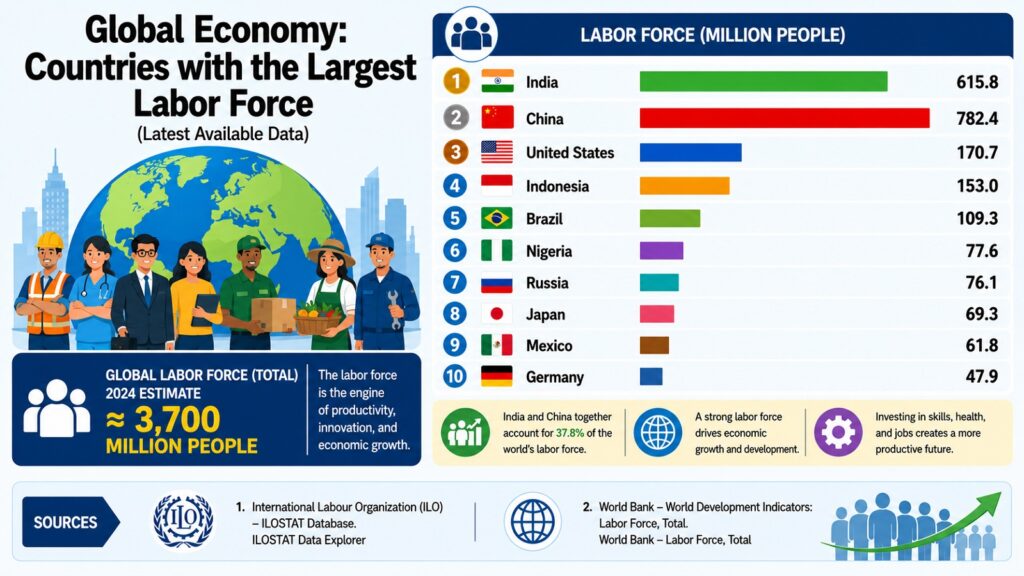

The global workforce is not simply the sum of all working people around the world. It is the collective human capital that drives economic progress, powers innovation, and delivers the productivity gains that raise living standards over time. Knowledge, skills, creativity, leadership, and entrepreneurship are the defining assets of any modern economy, and the quality of a country’s workforce determines its capacity to compete, adapt, and grow within the Global Economy.

Human capital theory, developed by economists Gary Becker and Theodore Schultz, established that investment in education, training, and workforce development generates economic returns comparable to physical capital investment, often higher. Countries that prioritize education, lifelong learning, and skills development consistently achieve greater productivity, higher wages, stronger innovation capacity, and more resilient economies than those that do not. This is not coincidence. It is a measurable relationship between human investment and economic output.

Talent mobility adds another dimension to how the global workforce shapes the Global Economy. When skilled professionals move across borders, they carry knowledge, networks, and entrepreneurial energy that can accelerate innovation in receiving economies. Silicon Valley, widely recognized as the world’s most productive technology innovation hub, has historically drawn a substantial share of its entrepreneurial talent from international immigrants, many of whom founded companies that went on to generate enormous economic value globally.

Demographic trends are creating new workforce pressures across the Global Economy. Aging populations in Europe, Japan, and parts of East Asia are reducing labor force participation, increasing pension and healthcare costs, and creating shortages in skilled occupations. Meanwhile, rapidly growing working-age populations in Sub-Saharan Africa and South Asia represent a significant demographic dividend if education and economic opportunity systems develop fast enough to absorb and develop this talent effectively.

The future of the global workforce is being reshaped by artificial intelligence, automation, and digital transformation. These technologies are eliminating routine and repetitive tasks while creating demand for higher-order cognitive skills, creative problem-solving, digital literacy, and adaptability. Economies and organizations that invest seriously in reskilling, continuous learning, and workforce adaptability are positioning themselves for sustainable competitive advantage in the evolving Global Economy.

Table 6: Eight Workforce Factors Driving the Global Economy

| Workforce Factor | Contribution to the Global Economy |

| Education and Skill Development | Builds human capital that drives productivity, innovation, and economic growth |

| Talent Mobility and Migration | Transfers skills and entrepreneurial energy across borders, accelerating innovation |

| Demographic Dividends | Young, growing workforces expand labor supply and support economic development |

| Digital Skills and Literacy | Enables workforce participation in technology-driven industries and processes |

| Lifelong Learning and Reskilling | Maintains workforce relevance as automation and AI transform labor markets |

| Leadership and Management Quality | Improves organizational performance, decision-making, and competitive positioning |

| Women’s Workforce Participation | Expands labor supply, boosts GDP, and improves household economic outcomes |

| Entrepreneurship and Innovation | Creates new businesses, industries, and employment opportunities globally |

6. Global Economy Through Global Resources

Natural resources are the physical foundation upon which the Global Economy rests. Energy, water, agricultural land, critical minerals, forests, fisheries, and biodiversity are not peripheral inputs. They are the raw materials from which industrial production, technological innovation, food security, and infrastructure development emerge. No economy, however advanced, has completely severed its dependence on natural resources. What has changed is how efficiently those resources are used and how equitably the benefits of their use are distributed.

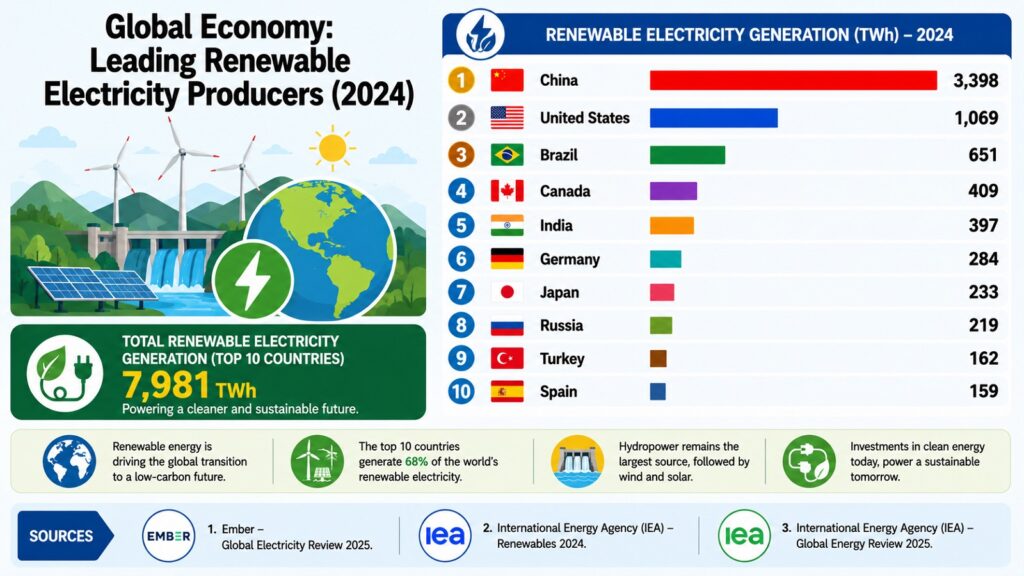

Energy resources illustrate this relationship particularly clearly. The industrialization of Western economies during the nineteenth and twentieth centuries was built substantially on coal and oil. The availability of affordable, reliable energy enabled manufacturing expansion, transportation development, agricultural mechanization, and the kind of sustained productivity growth that raised living standards across the developed world. Today, the transition toward renewable energy is reshaping resource economics at a global scale, with significant consequences for trade flows, geopolitics, and industrial competitiveness.

Critical minerals such as lithium, cobalt, and rare earth elements have emerged as strategic resources in the era of electric vehicles, renewable energy, and advanced electronics. Their concentration in a small number of countries creates supply chain vulnerabilities that increasingly influence foreign policy, trade agreements, and investment decisions. The International Energy Agency has warned that demand for critical minerals could increase by as much as six times by 2040, making resource access a defining economic challenge for the coming decades.

Norway offers a compelling case study in responsible resource management. The country built its sovereign wealth fund by channeling revenues from North Sea oil production into a long-term savings vehicle rather than short-term public spending. This discipline transformed finite resource wealth into permanent financial wealth that now supports Norwegian citizens across generations, demonstrating that resource abundance can translate into sustained prosperity when managed wisely.

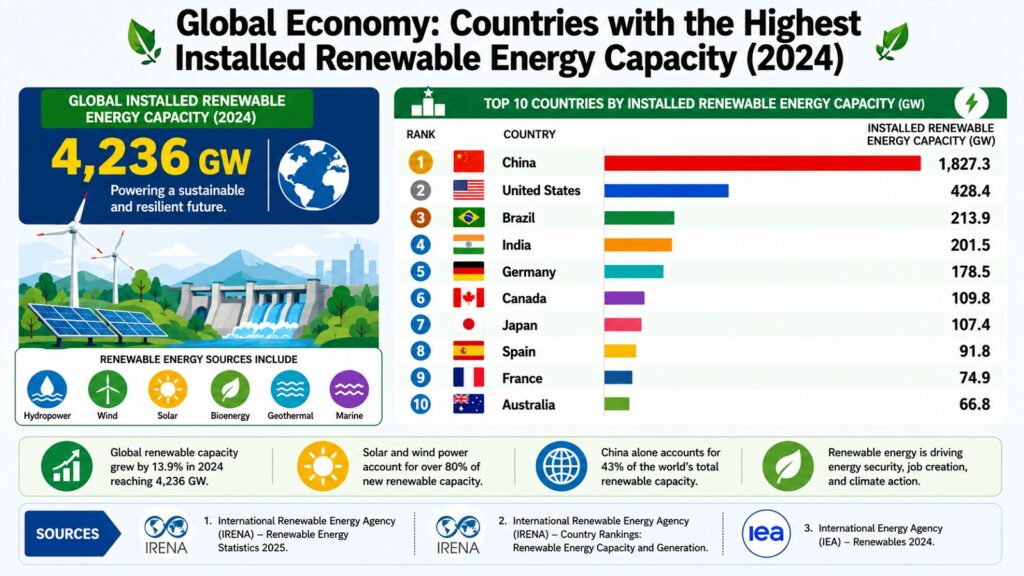

The future of global resources is being reshaped by renewable energy adoption, circular economy practices, and technological efficiency improvements. Solar and wind energy are becoming the lowest-cost sources of new electricity generation in many parts of the world, reducing dependence on fossil fuels and altering long-standing patterns of resource trade. Circular economy principles, which emphasize designing out waste and keeping materials in productive use, are gaining traction as businesses and governments recognize that resource efficiency is both an environmental and competitive imperative.

Table 7: Eight Resource Categories Supporting the Global Economy

| Resource Category | Contribution to the Global Economy |

| Energy Resources (Oil, Gas) | Power industrial production, transportation, and electricity generation globally |

| Renewable Energy (Solar, Wind) | Provide clean, increasingly cost-competitive alternatives supporting energy transition |

| Critical Minerals (Lithium, Cobalt) | Enable electric vehicles, clean energy technology, and advanced electronics production |

| Water Resources | Support agriculture, manufacturing, urban development, and population health globally |

| Agricultural Land and Food Systems | Ensure food security and underpin rural economies across the developing world |

| Forests and Biodiversity | Provide carbon sequestration, ecosystem services, and biodiversity support systems |

| Fisheries and Marine Resources | Supply protein and livelihoods for billions, especially in coastal developing economies |

| Rare Earth Elements | Essential for high-tech manufacturing, defence systems, and advanced digital devices |

7. Global Economy Through Global Economic Governance

Without governance, the Global Economy would be an ungoverned market in which the powerful consistently exploit the weak, financial crises spread without check, and trade disputes descend into damaging confrontations. Global economic governance is the institutional framework of rules, policies, agreements, and organizations that enables the world economy to function with reasonable efficiency, transparency, and predictability. It is not glamorous, but it is indispensable.

Economic governance operates at multiple levels simultaneously. National governments set fiscal and monetary policies that determine tax rates, public spending priorities, interest rates, and exchange rate management. Central banks manage domestic financial stability while coordinating with international counterparts through institutions like the Bank for International Settlements. International organizations such as the World Trade Organization, International Monetary Fund, and World Bank provide multilateral frameworks for trade rules, financial support, and development assistance that extend governance beyond national borders.

The importance of coordinated governance becomes clearest during crises. During the 2008 global financial crisis, the G20 nations coordinated stimulus spending, bank recapitalization measures, and regulatory reforms in ways that prevented a global recession from becoming a global depression. The rapid coordination of the G20, unusual in its speed and ambition, demonstrated that collective governance action can meaningfully limit economic damage when international cooperation is genuinely prioritized.

Tax policy has emerged as a particularly significant governance challenge in the modern Global Economy. Multinational corporations have historically been able to shift profits toward low-tax jurisdictions, reducing their effective tax rates substantially below statutory rates in the countries where they generate revenue. The OECD-led initiative on a global minimum corporate tax rate of fifteen percent, agreed upon by over one hundred and thirty countries in 2021, represents a significant attempt to modernize international tax governance in ways that better reflect how twenty-first-century business actually operates.

Effective governance also creates the enabling conditions for sustainable business investment. Clear property rights, enforceable contracts, transparent regulation, and predictable monetary policy reduce the uncertainty and transaction costs that inhibit investment and growth. Governance quality is consistently one of the strongest predictors of long-run economic development, explaining much of the variation in prosperity between countries with similar resource endowments.

Table 8: Eight Governance Mechanisms Supporting the Global Economy

| Institution / Mechanism | Contribution to the Global Economy |

| World Trade Organization | Sets and enforces international trade rules, reducing barriers and dispute risks |

| International Monetary Fund | Provides financial support and macroeconomic policy guidance to member countries |

| World Bank Group | Funds infrastructure and development projects reducing poverty and building capacity |

| G20 Nations Forum | Coordinates major economies on financial stability and shared global challenges |

| Central Bank Networks | Manage monetary policy and coordinate during financial stability crises internationally |

| OECD Global Minimum Tax | Reduces corporate profit-shifting and creates fairer international tax competition |

| Regional Trade Agreements | Establish preferential trade rules within geographic blocs, deepening economic integration |

| Competition Policy and Regulation | Prevents monopolistic practices and maintains fair market conditions within economies |

8. Global Economy Through Sustainable Economy

The idea that economic growth and environmental responsibility are fundamentally incompatible has given way to a more sophisticated understanding. A Sustainable Economy does not trade prosperity for protection. It builds long-term prosperity by integrating responsible resource use, social development, and technological innovation into the core logic of economic activity. This shift in thinking is increasingly reflected in investment decisions, government policy, corporate strategy, and international agreements.

Sustainable development gained its most influential modern expression in the Brundtland Commission’s 1987 report, which defined it as meeting the needs of the present without compromising the ability of future generations to meet their own needs. In practical terms, this means economic systems must find ways to generate growth without permanently depleting the natural systems and social foundations that make growth possible in the first place.

The business case for sustainability has become substantially clearer over the past decade. Companies that score well on environmental, social, and governance criteria have demonstrated lower financing costs, stronger talent attraction, reduced regulatory risk, and more resilient long-run financial performance than those that ignore sustainability considerations. BlackRock, the world’s largest asset manager, has publicly stated that sustainable investment frameworks are central to how it evaluates long-term risk and return, reflecting a broader institutional shift that is channeling enormous capital flows toward sustainable business models.

Denmark provides a compelling national case study. Through sustained public and private investment in wind energy technology beginning in the 1980s, Denmark transformed itself from an oil-dependent economy into a global leader in renewable energy. Danish companies like Vestas became world-leading wind turbine manufacturers, creating export earnings, high-quality employment, and technological leadership from what began as an environmental and energy security initiative. This demonstrates that sustainable investment creates competitive economic advantage, not merely environmental benefit.

The transition to a Sustainable Economy presents genuine implementation challenges. The capital requirements for renewable energy infrastructure, clean transportation, and sustainable agriculture are enormous. Policy coordination across competing national interests remains difficult. Technological solutions for the hardest-to-decarbonize sectors, including heavy industry, shipping, and aviation, are still maturing. These challenges are real, but they are also business opportunities for the companies and countries that develop credible solutions.

Table 9: Eight Sustainability Drivers Shaping the Global Economy

| Sustainability Principle / Driver | Contribution to the Global Economy |

| Renewable Energy Transition | Reduces fossil fuel dependence and builds long-term energy security and competitiveness |

| Circular Economy Principles | Minimize waste and keep materials in productive use, reducing costs and resource dependence |

| ESG Investment Frameworks | Channel capital toward sustainable businesses, reducing systemic financial and climate risk |

| Carbon Pricing Mechanisms | Internalize environmental costs, incentivizing businesses to reduce emissions efficiently |

| Sustainable Finance and Green Bonds | Fund low-carbon infrastructure and sustainable development at scale internationally |

| Climate Resilience Investment | Reduces long-term economic damage from climate-related disruptions and physical risks |

| Clean Technology Innovation | Creates new industries, export opportunities, and competitive advantages globally |

| Sustainable Agriculture Systems | Improve food security, reduce land degradation, and support rural economic development |

Conclusion: The Future of the Global Economy and Global Growth

The eight forces explored in this article do not operate independently. They form a dynamic, interconnected system in which each force depends upon and amplifies the others. Global trade creates demand for global finance. Global production requires both global resources and a skilled global workforce. Global innovation is shaped by governance and accelerated by sustainable investment. Understanding these relationships transforms information about the Global Economy into genuine strategic insight.

For businesses, decisions about where to produce, how to finance growth, which markets to enter, and which technologies to adopt are embedded within a global context that must be understood rather than ignored. Companies that outperform consistently are those that read global economic signals accurately, adapt strategies quickly, and build capabilities to compete across multiple markets.

For governments, policies affecting trade, education, infrastructure, and sustainability do not operate in isolation. They interact with decisions of businesses, investors, and international institutions in ways that compound or undermine their effects. Effective governance means designing with systemic complexity in mind, not optimizing for short-term objectives.

For individuals and students, understanding the Global Economy provides a framework for interpreting the forces shaping career opportunities, investment environments, and societal change. In a world where conditions shift rapidly, analytical fluency in global economic forces is a durable competitive advantage.

The Global Economy will continue to evolve in ways that cannot be predicted precisely. Geopolitical realignments, technological breakthroughs, demographic shifts, and environmental pressures will create new challenges and new opportunities. What will not change is that the world’s economies are deeply interconnected, and that success requires continuous learning, strategic adaptability, and commitment to sustainable growth.

The organizations, governments, and individuals who thrive in the future Global Economy will be those who understand not just what is happening, but why it is happening and what it demands.

Table 10: Eight Strategic Lessons About the Global Economy

| Strategic Lesson | Application for Businesses, Governments, and Individuals |

| Trade Creates Opportunity | Businesses that access global markets outperform those limited to domestic demand |

| Finance Enables Growth | Access to diverse capital sources strengthens investment capacity and business resilience |

| Production Must Be Resilient | Diversified supply chains reduce vulnerability to disruption and improve long-term stability |

| Innovation Drives Competitiveness | Sustained R&D and technology adoption are essential for long-run business success |

| Workforce Quality Determines Outcomes | Investment in education and skills consistently outperforms resource or geographic advantage |

| Resource Efficiency Is Strategic | Managing natural resources responsibly creates competitive and long-term economic advantage |

| Governance Shapes Prosperity | Stable institutions, clear rules, and policy consistency attract investment and support growth |

| Sustainability Is a Business Imperative | ESG practices reduce risk, lower capital costs, and improve long-term business performance |