Table of Contents

Introduction: Capital Structure as the Foundation of Corporate Finance

Every business decision, from launching a product line to acquiring a competitor, eventually comes down to one fundamental question: how will we pay for it? That question sits at the heart of capital structure. It is not simply a financial concept found in textbooks. It is the strategic backbone of every functioning corporation, shaping how businesses grow, survive difficult periods, and reward the people who invest in them.

Capital structure refers to the way a corporation finances its operations and growth through a combination of debt and equity. But that definition barely scratches the surface. In practice, capital structure is a living, evolving framework that reflects a company’s priorities, risk tolerance, market environment, and long-term ambitions. It is one of the most important aspects of the modern business ecosystem. Corporations that manage their capital structure well tend to grow faster, attract better investors, and weather economic storms more effectively than those that ignore it.

The choices embedded in capital structure reach far beyond balance sheets. They influence how confident shareholders feel about the future of a company. They affect how easily a business can borrow money during periods of expansion. They determine whether a corporation can sustain operations when revenues fall unexpectedly. Capital structure shapes decisions about dividends, acquisitions, research investment, and even hiring.

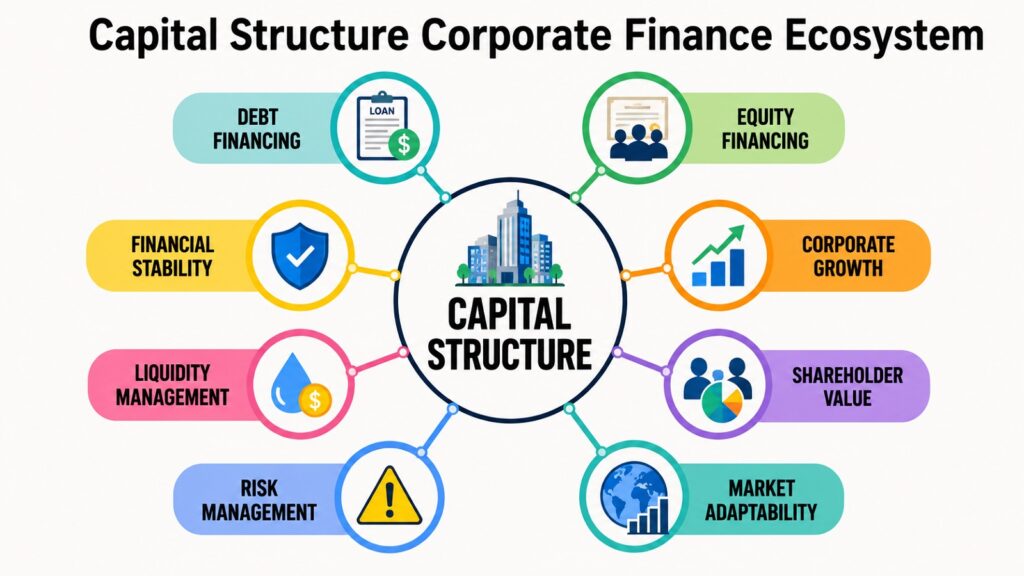

This article examines the eight fundamental pillars that characterize capital structure in contemporary corporate finance. Each pillar uncovers a unique aspect of how organizations handle their financing choices, balance growth with stability, and prepare for sustained success. Grasping these pillars offers a more comprehensive understanding of how companies function beyond the superficial indicators of earnings reports and stock valuations. Whether you are an investor, a business expert, or an individual seeking to comprehend the intricacies of corporate finance, this guide provides a practical and enlightening foundation.

Capital Structure: 8 Pillars at a Glance

| Capital Structure Pillars | Strategic Relevance to Capital Structure |

| Debt vs Equity Financing | Determines how growth is funded and how ownership is balanced against borrowing |

| Cost of Capital Optimization | Guides companies toward the most efficient financing mix to reduce funding costs |

| Financial Risk Management | Links financing decisions to solvency, leverage exposure, and operational resilience |

| Corporate Growth Financing | Enables expansion, acquisitions, and market entry through structured financing |

| Shareholder Value Creation | Connects financing strategy to investor returns, valuation, and market confidence |

| Liquidity Stability | Supports cash flow continuity and debt servicing capacity across market cycles |

| Business Lifecycle Adaptation | Shows how financing priorities shift from startup to maturity to restructuring |

| Market Conditions Response | Explains how interest rates, credit availability, and economic cycles shape financing |

1. Capital Structure and Debt vs Equity Financing

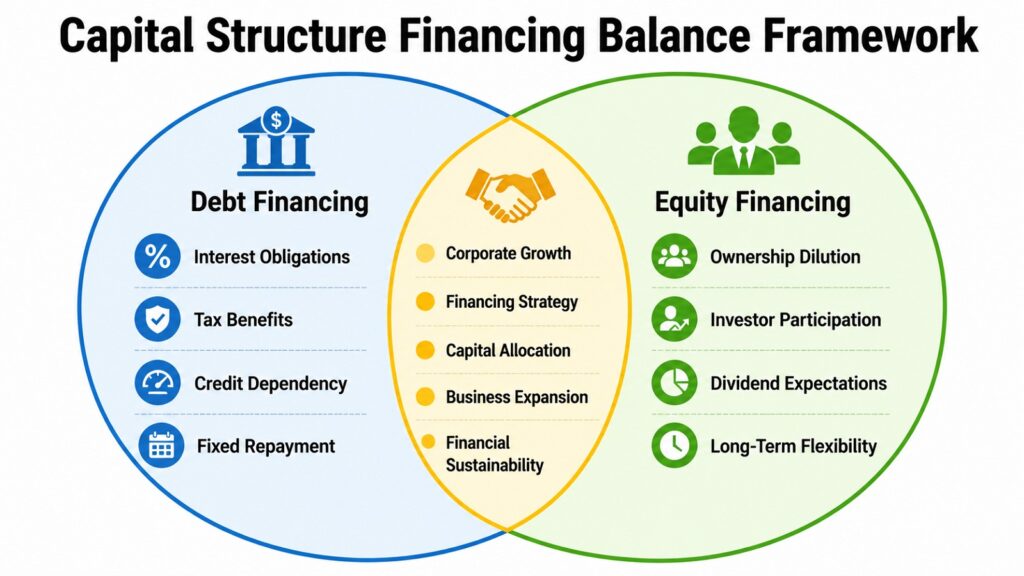

At the core of every capital structure conversation is a choice between two broad paths: borrow money or invite investors. These are debt financing and equity financing, and corporations spend enormous energy deciding how to balance them. Neither option is universally better. Each carries advantages that can power a company forward and drawbacks that can slow it down if mismanaged.

Debt financing means a company raises funds by borrowing, typically through bank loans, bonds, or credit facilities. The lender receives interest payments over time, and the company retains full ownership. This works well when a business generates steady cash flows strong enough to cover repayment obligations. Leverage can amplify returns when things go well because shareholders benefit from growth funded without giving up any ownership stake.

Equity financing works differently. A corporation raises funds by selling ownership stakes to investors through private placements, venture funding, or public offerings. There is no mandatory repayment, which improves financial flexibility and reduces the immediate pressure that comes with fixed interest costs. However, every share issued dilutes the value of existing ownership and spreads earnings per share across a larger base. For founders and early shareholders, this trade-off requires careful thought.

The practical decision between debt and equity is rarely black and white. Companies consider their current debt load, cash flow predictability, growth opportunities, tax environment, and investor expectations before committing to either path. Interest payments on debt are typically tax-deductible, which makes borrowing cheaper in practice than its headline rate suggests. On the other hand, too much debt creates fragility. When revenue drops or interest rates rise, heavily leveraged companies can find themselves in serious trouble.

Most corporations use a combination of both. The goal is to find a financing structure that keeps capital costs manageable, preserves ownership where it matters, and maintains enough flexibility to respond to changing conditions. Capital structure is about balance, not extremes.

Capital Structure: Debt vs Equity Financing Comparison

| Financing Factor | Impact on Capital Structure |

| Ownership retention | Debt preserves ownership; equity dilutes existing shareholder stakes |

| Repayment obligation | Debt requires fixed payments; equity carries no mandatory repayment |

| Tax treatment | Interest on debt is usually tax-deductible, reducing effective borrowing costs |

| Risk exposure | Higher debt increases financial risk during revenue downturns or rate hikes |

| Growth acceleration | Leverage can amplify returns when deployed in high-return investment opportunities |

| Investor dilution | Equity issuance spreads earnings per share across a wider ownership base |

| Flexibility under stress | Equity-heavy structures provide more breathing room during economic downturns |

| Capital cost dynamics | Blended financing optimizes WACC by combining cheaper debt with equity stability |

2. Capital Structure and Cost of Capital Optimization

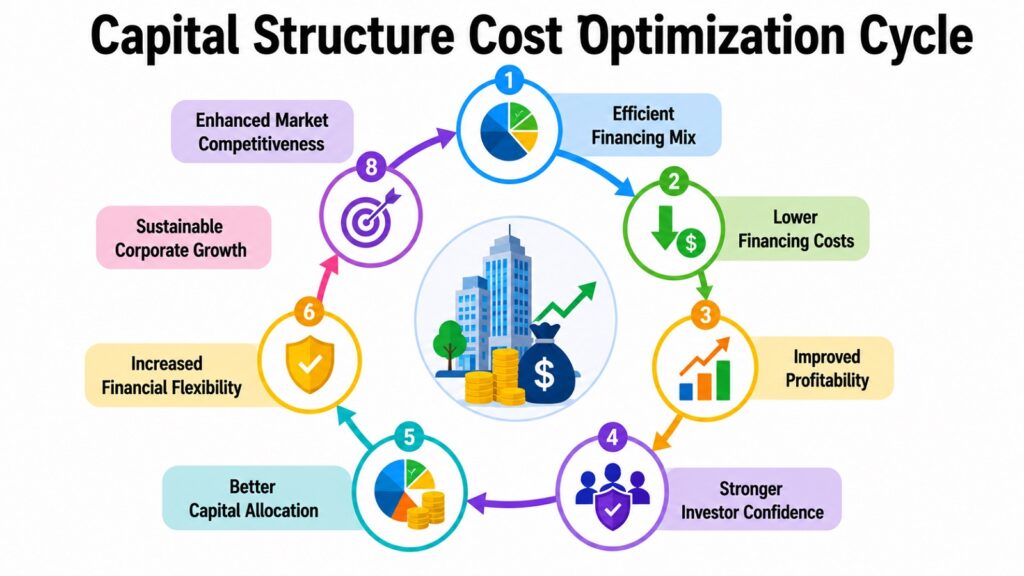

Every dollar a company raises has a price attached to it. That price is the cost of capital, and how well a corporation manages it can determine the difference between a profitable business and one that struggles to grow. Capital structure is one of the most powerful tools available to corporate leaders trying to reduce this cost while maintaining enough financial flexibility to pursue opportunities.

When companies raise money through a mix of debt and equity, the blended cost of those funds is known as the Weighted Average Cost of Capital, or WACC. A lower WACC means the company generates returns above a smaller threshold, which increases the value it creates for shareholders. Businesses with well-optimized capital structures can invest in growth at lower hurdle rates than rivals with inefficient financing.

Optimizing cost of capital is not about minimizing debt or maximizing equity. It is about finding the right blend. Debt is typically cheaper than equity because lenders take on less risk than shareholders and because interest payments are tax-deductible. However, adding more debt increases financial risk, which in turn raises the return demanded by equity investors. At some point, the cost savings from cheap debt are offset by rising equity costs. Smart capital structure management finds the zone before that point is reached.

Corporate leaders think about this through the lens of investor expectations. Shareholders expect returns that reflect the risk of holding equity in a business. Bondholders expect returns tied to credit quality. When companies communicate their financing strategy clearly and demonstrate financial discipline, investor confidence tends to improve, lowering the return premium investors demand.

Companies also consider capital allocation decisions carefully. Raising equity when stock prices are high can be a cost-effective way to fund growth. Issuing bonds when credit spreads are tight locks in cheap long-term financing. Efficient capital structure is as much about strategic timing as it is about balance sheet mechanics.

Capital Structure: Key Factors in Cost of Capital Optimization

| Factor | Effect on Capital Structure Efficiency |

| WACC level | Lower WACC increases project viability and boosts overall company valuation |

| Debt tax shield | Tax-deductible interest reduces the effective cost of borrowing for the business |

| Equity risk premium | Higher perceived risk raises the return demanded by shareholders, increasing equity cost |

| Credit rating | Stronger credit ratings allow access to cheaper debt with more favorable terms |

| Financing timing | Raising capital during favorable market conditions reduces the overall cost of funds |

| Investor communication | Clear financial strategy builds confidence and reduces the risk premium investors apply |

| Capital allocation discipline | Deploying funds into high-return projects improves return on invested capital |

| Leverage ratio management | Balancing debt levels avoids the point where rising equity costs offset debt savings |

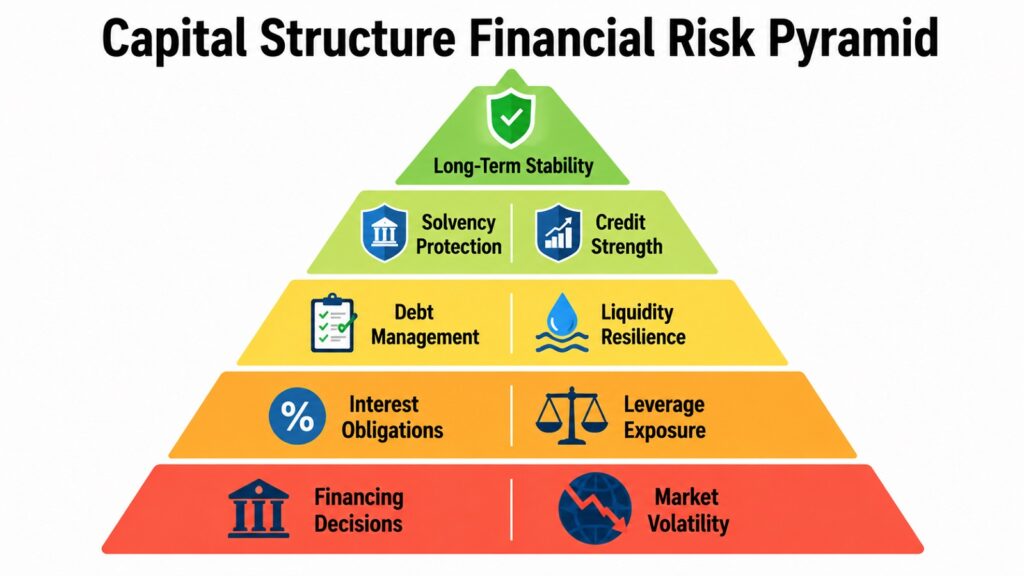

3. Capital Structure and Financial Risk Management

The ambition for growth and the associated financial risks are closely linked. When companies take on debt to grow, they incur obligations that must be fulfilled, irrespective of whether their revenue meets expectations. Consequently, capital structure is intrinsically tied to risk management strategies. The manner in which a company finances its operations influences its susceptibility to adverse conditions and its ability to withstand unexpected challenges.

Debt introduces leverage into a business, and leverage is a double-edged instrument. When operating profits are rising, leverage amplifies returns to shareholders because interest payments remain fixed while the company captures additional profit above those obligations. However, when revenues fall or costs spike unexpectedly, those same fixed obligations can become suffocating. Companies that entered aggressive leverage cycles before economic downturns, such as during the 2008 financial crisis, found themselves unable to service debt even while core operations remained viable.

Interest burden is one of the most immediate financial risks associated with capital structure. If a company carries substantial variable-rate debt and interest rates rise sharply, its financing costs can increase significantly within a short timeframe. Fixed-rate long-term debt provides more predictability but usually comes at a higher initial cost. Corporations manage this risk by structuring debt maturities carefully, diversifying between fixed and variable rates, and maintaining revolving credit facilities that provide liquidity buffers.

Liquidity risk and solvency risk are related but distinct. Liquidity risk means a company cannot meet short-term obligations because cash is unavailable, even if the business itself is fundamentally solvent. Solvency risk is more existential, meaning total liabilities exceed the value of assets. Capital structure decisions directly influence both dimensions.

Conservative capital structures provide a cushion against these pressures. Lower leverage means smaller mandatory payments and more room to absorb revenue shocks. The art of capital structure lies in calibrating financial risk to match the actual risk profile of the business, not defaulting to either extreme.

Capital Structure: Major Financial Risk Factors

| Risk Factor | Business Impact |

| Excessive leverage | Fixed debt obligations reduce flexibility when revenues fall or costs rise unexpectedly |

| Interest rate exposure | Variable-rate debt increases financing costs when broader interest rates move higher |

| Refinancing risk | Large near-term maturities create vulnerability if credit markets tighten or dry up |

| Liquidity pressure | Insufficient cash reserves make it difficult to meet short-term obligations on time |

| Covenant breach | Debt covenants can restrict operations or trigger defaults when financial ratios deteriorate |

| Credit rating downgrade | Weaker credit ratings raise borrowing costs and limit access to capital markets |

| Earnings volatility | Companies with cyclical revenues face greater risk when leverage is high during downturns |

| Bankruptcy risk | Sustained insolvency or inability to service debt can lead to restructuring or liquidation |

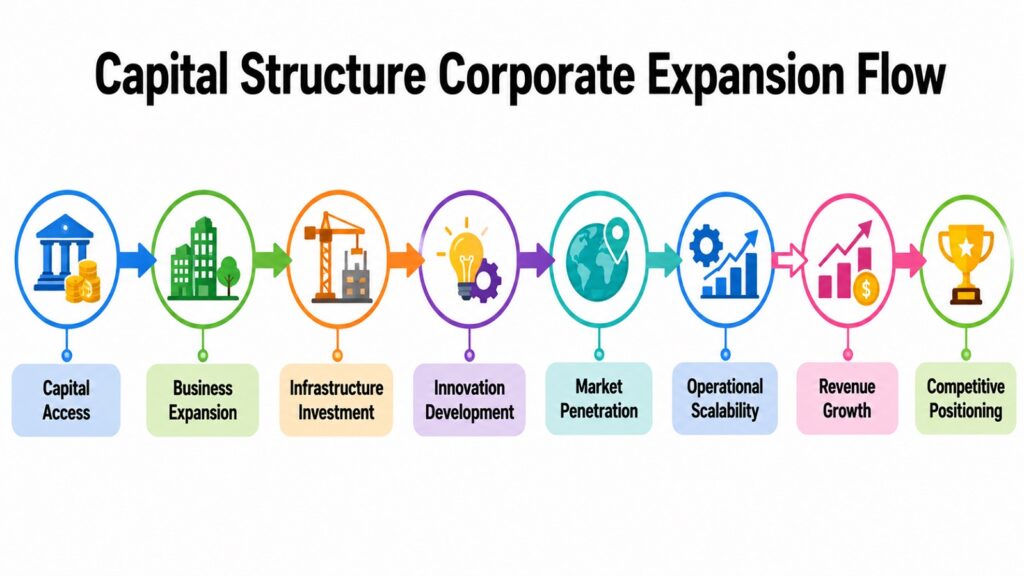

4. Capital Structure and Corporate Growth Financing

Growth does not happen by accident. Behind every major corporate expansion, every acquisition, every product launch at scale, there is a financing structure that made it possible. Capital structure is the mechanism through which companies translate strategic ambitions into funded reality. Understanding how businesses use their financing mix to support growth reveals much about the quality and sustainability of their expansion strategies.

Corporations pursue growth along several axes simultaneously. They invest in new geographic markets, fund research and development programs, build manufacturing capacity, acquire competitors, and develop technology platforms. Each of these objectives requires capital, and the way that capital is sourced matters. A company that funds aggressive expansion exclusively through short-term debt while ignoring equity options may grow quickly in the short term but create fragility that limits its resilience later.

Financing for acquisitions serves as a significant indicator of capital structure strategy. When a firm opts to acquire another entity, it must determine whether to utilize available cash, issue new equity, take on debt, or employ a combination of these methods. Each option has ramifications for financial leverage, earnings per share, returns for shareholders, and costs associated with integration. Major leveraged buyouts, where acquiring firms heavily finance against the assets of the target company, have resulted in both remarkable successes and notable failures, contingent upon the effectiveness of post-acquisition cash flows in servicing the incurred debt.

Infrastructure investment and technology development require patient, long-duration financing. Companies building manufacturing plants, data centers, or distribution networks often use long-term bonds or structured project finance to match the lifespan of the assets being funded. This alignment between asset duration and financing duration is a key principle of sound capital structure management. Mismatches, such as funding long-term assets with short-term debt, create refinancing risks that can destabilize otherwise healthy businesses.

Sustainable growth financing also involves maintaining investor confidence throughout the expansion cycle. Companies that demonstrate disciplined use of borrowed capital and show clear paths to return on investment tend to attract better financing terms and broader investor support.

Capital Structure: Growth Financing Activities

| Business Objective | Capital Structure Relevance |

| Geographic expansion | Requires durable capital allocation matched to market entry timelines and risks |

| Acquisition strategy | Financing mix affects leverage, dilution, and post-acquisition cash flow stability |

| Research and development | Long-term equity or retained earnings support uncertain investment timelines |

| Manufacturing capacity | Long-duration bonds align financing lifespan with asset depreciation cycles |

| Technology platform development | Patient capital through equity or structured debt supports multi-year build cycles |

| Market share growth | Competitive financing allows lower pricing and sustained investment in customer acquisition |

| Talent and human capital | Equity compensation reduces cash outflow while aligning employees with growth goals |

| Working capital scaling | Credit facilities and revolving lines fund operational growth without diluting equity |

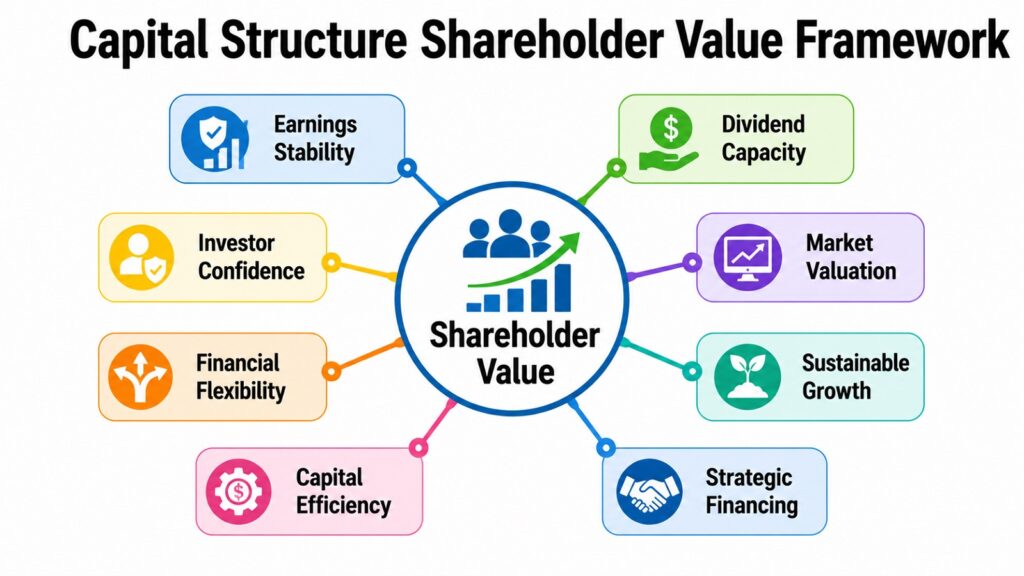

5. Capital Structure and Shareholder Value Creation

Shareholders invest in companies expecting returns that justify the risks they accept. Capital structure plays a central role in whether those expectations are met. The way a corporation finances itself influences its profitability, valuation, dividend capacity, and market credibility in ways that investors scrutinize closely. Poor financing decisions can erode trust and compress valuations even when the underlying business performs reasonably well.

One of the most direct connections between capital structure and shareholder value runs through earnings per share. When a company issues new equity, it increases total shares outstanding. Unless the investment generates returns above the cost of that new capital quickly, earnings per share declines for existing shareholders. Companies with strong return track records can justify equity issuance more easily.

Debt, used appropriately, can actually enhance shareholder value. By financing operations partially through borrowed capital, a company can amplify equity returns when business performance is strong. The tax deductibility of interest payments further improves this dynamic by reducing the effective cost of debt financing. Share buyback programs, often funded through debt, have become one of the most common mechanisms through which corporations return value to shareholders while maintaining leverage within acceptable ranges.

Dividend policy is closely tied to capital structure as well. Companies with stable, lower-leverage financing structures tend to sustain consistent dividend payments, which attracts income-focused investors and provides a signal of financial health. Businesses carrying heavy debt burdens may struggle to maintain dividends during difficult periods, damaging their reputation with institutional investors who rely on consistent income. The relationship between financing strategy and dividend sustainability is a real and important part of shareholder value management.

Beyond financial metrics, capital structure sends signals to the market about management confidence. A company that increases its debt load to fund an acquisition is signaling conviction about future cash flow. Investors interpret these signals carefully, and they shape stock price performance over time.

Capital Structure: Shareholder Value Factors

| Financial Factor | Influence on Investors or Valuation |

| Earnings per share | Equity dilution from new share issuance reduces per-share earnings for existing investors |

| Leverage and ROE | Appropriate debt amplifies equity returns when investment performance exceeds borrowing costs |

| Dividend sustainability | Lower leverage supports consistent dividend payments, attracting income-focused investors |

| Share buybacks | Debt-funded buybacks reduce share count and concentrate ownership value for remaining holders |

| Tax efficiency | Interest deductions from debt reduce taxable income, improving net returns to shareholders |

| Investor signaling | Financing decisions communicate management confidence and strategic direction to the market |

| Valuation multiples | Efficient capital structures support higher price-to-earnings and enterprise value multiples |

| Credit profile | Strong balance sheet management reduces financial risk and attracts higher-quality investors |

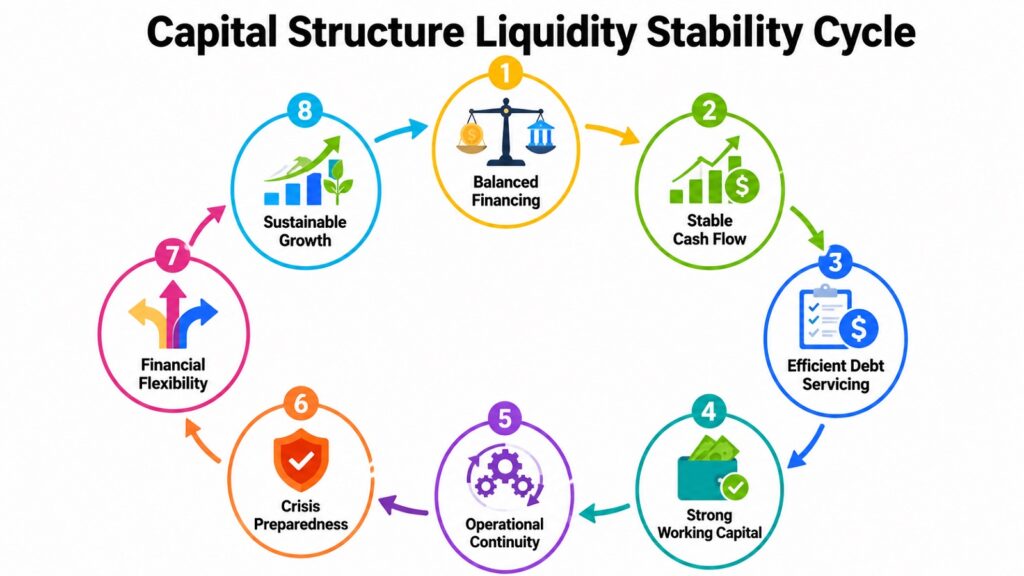

6. Capital Structure and Liquidity Stability

A company can be profitable on paper and still collapse if it runs out of cash. Liquidity, the ability to meet financial obligations as they come due, is a separate but deeply connected dimension of capital structure. How a corporation structures its financing determines not just its growth potential but its operational survival capacity during periods of stress. Capital structure decisions that ignore liquidity dynamics often produce visible problems during economic disruptions.

The relationship between debt maturity and liquidity is particularly important. Companies that fund long-term operations with short-term borrowing create a structural vulnerability. When those short-term obligations come due, the business must either repay them or find new lenders willing to extend credit. During normal market conditions this refinancing process is routine. During periods of credit market stress, it can become extremely difficult, forcing companies into asset sales, operational cutbacks, or worse.

Working capital management sits at the intersection of capital structure and daily liquidity. Businesses that carry large inventories, extend long payment terms to customers, or face slow collections from receivables require more working capital financing than those with lean, fast-turning operational models. Companies in industries with long production cycles often use revolving credit facilities to bridge the gap between when cash leaves the business and when it returns. The availability and cost of these facilities is directly influenced by the company’s overall capital structure and creditworthiness.

Cash reserves provide a form of insurance against liquidity shocks. Technology companies often hold substantial cash balances as a buffer against unpredictable revenue swings. However, holding excess cash has a cost, since that capital could be deployed in operations or used to reduce expensive debt. The optimal reserve level reflects business model risk and revenue predictability.

Capital Structure: Liquidity Stability Factors

| Liquidity Factor | Strategic Importance |

| Debt maturity profile | Short-term maturities create refinancing pressure during credit market disruptions |

| Revolving credit facilities | Provide flexible access to cash for operational needs without permanent capital commitment |

| Cash reserve levels | Offer a buffer against revenue shocks but must be balanced against deployment efficiency |

| Working capital cycle | Longer cycles require more financing to bridge gaps between cash outflows and inflows |

| Interest coverage ratio | Measures ability to service debt from operating earnings, signaling solvency health |

| Debt covenant compliance | Breaching financial covenants can restrict liquidity access or accelerate repayment |

| Funding source diversification | Multiple financing sources reduce dependency on any single lender or market condition |

| Free cash flow generation | Strong operating cash flow reduces reliance on external financing during stress periods |

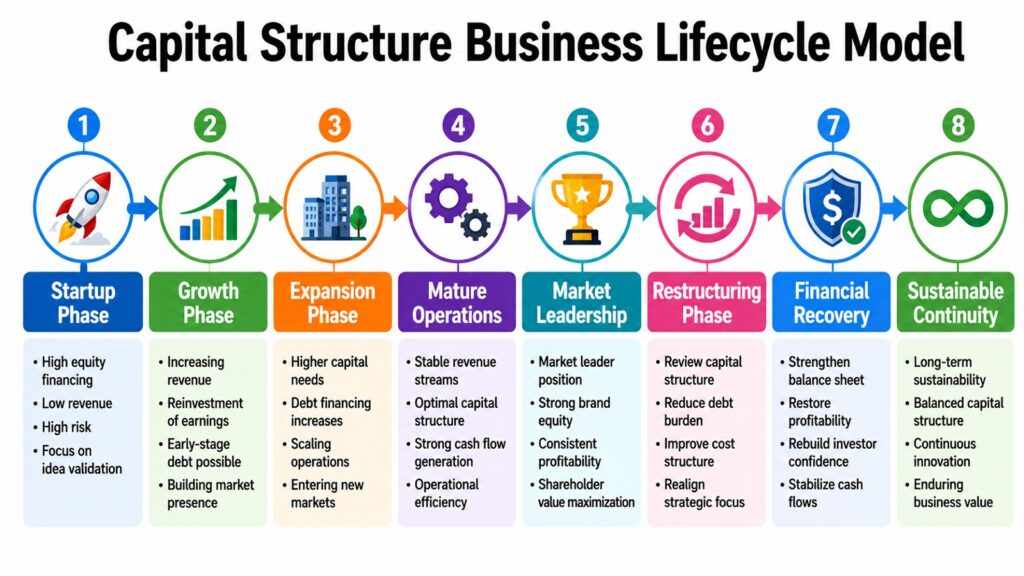

7. Capital Structure Across the Business Lifecycle

A financing strategy that works for a startup rarely makes sense for a mature corporation. Capital structure is not static. It evolves as businesses grow, mature, and sometimes face the difficult work of restructuring or turning around declining operations. Understanding how financing priorities shift across different lifecycle stages helps explain why two companies in the same industry can carry very different balance sheet compositions.

Early-stage companies face a fundamental challenge: they need capital to grow but have little operating history to attract lenders. Most startups rely primarily on equity financing, sourcing funds from founders, angel investors, and venture capital firms. Debt is limited at this stage because lenders want predictable repayment capacity that young companies rarely demonstrate.

As companies enter the growth stage, they begin to generate revenues and sometimes profits, which opens access to more structured financing. Venture debt, revenue-based financing, and eventually bank credit become available. The capital structure begins to diversify. Growth-stage companies must balance the temptation to use cheap debt for faster expansion against the risk of taking on obligations before their financial model has been fully proven. Misjudging this balance has ended many promising growth companies.

Mature corporations operate with the most sophisticated capital structures. They have established cash flows, strong credit ratings, and access to deep capital markets. These companies use bonds, revolving credit facilities, and retained earnings alongside equity to fund operations. The objective at this stage shifts from growth acceleration to capital efficiency.

Financially distressed companies face the most acute capital structure challenges. When debt obligations exceed the capacity of business cash flows to service them, companies must consider restructuring their balance sheets through debt extensions, debt-to-equity conversions, or asset sales. Those who managed leverage conservatively during healthy periods tend to have more options.

Capital Structure: Business Lifecycle Financing Approaches

| Lifecycle Stage | Financing Approach |

| Seed stage | Founder capital and angel investment fund early operations with minimal or no debt |

| Venture-backed startup | Equity-heavy structure using venture capital rounds to fund growth and development |

| Growth stage | Combination of equity rounds and early-stage debt as revenues begin to emerge |

| Pre-IPO company | Structured financing and mezzanine debt prepare balance sheet for public market scrutiny |

| Publicly listed growth company | Mix of equity, convertible instruments, and selective debt for market expansion |

| Mature corporation | Optimized WACC through balanced debt and equity with focus on capital efficiency |

| Declining business | Conservative cash management and debt reduction to preserve operational flexibility |

| Distressed restructuring | Debt-to-equity conversion, asset sales, and renegotiated terms to restore solvency |

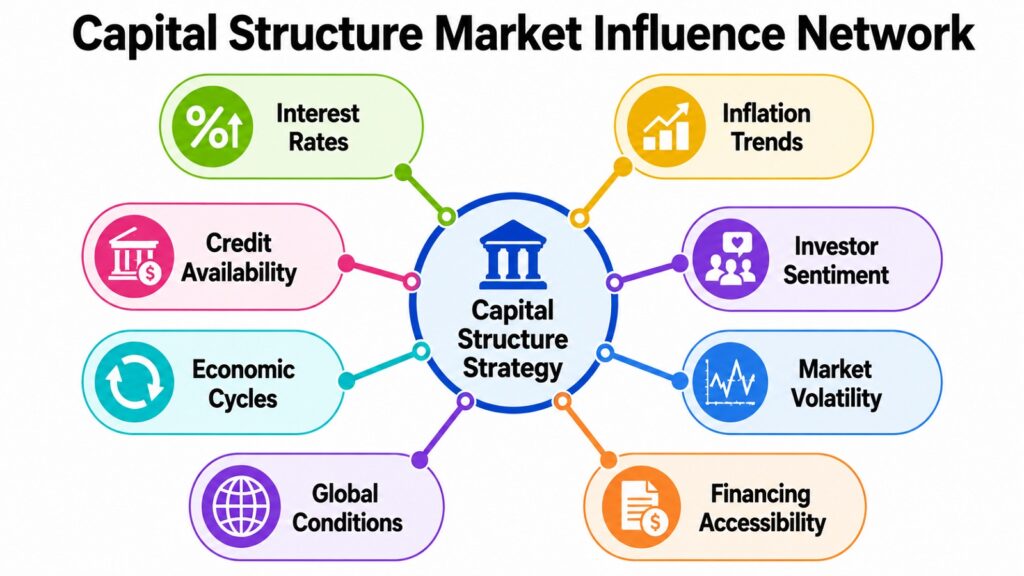

8. Capital Structure and Market Conditions

No capital structure decision is made in isolation from the broader economic environment. Interest rates, inflation dynamics, credit availability, investor sentiment, and the overall direction of the economic cycle all shape the financing choices that corporations make. Companies that treat capital structure as a fixed internal policy without accounting for external conditions often pay more for their capital and carry more risk than necessary.

Interest rates are perhaps the single most influential external variable in capital structure decision-making. When rates are low, borrowing becomes relatively inexpensive, encouraging companies to use debt more aggressively. The decade following the 2008 financial crisis saw historically low interest rates globally, which led to substantial increases in corporate debt levels as businesses refinanced existing obligations and funded expansion at very low costs. When central banks began raising rates aggressively starting in 2022 to combat inflation, the financing environment shifted rapidly and companies carrying floating-rate debt found their interest expenses rising significantly.

Inflation affects capital structure in multiple ways. Rising input costs squeeze operating margins, reducing the cash available to service debt. Companies with strong pricing power and well-structured fixed-rate debt tend to navigate inflationary periods better than those with narrow margins and variable financing costs.

Investor sentiment also shapes capital structure opportunities. During bull markets, equity issuance becomes attractive because share prices are higher, meaning companies raise more capital per share sold. Conversely, during market downturns, equity issuance becomes dilutive, pushing companies toward debt markets. Reading market conditions and timing capital structure decisions accordingly is a legitimate part of corporate finance strategy.

Capital Structure: Key Market Conditions and Financing Impact

| Market Condition | Impact on Financing Strategy |

| Low interest rate environment | Encourages higher leverage and debt refinancing to lock in cheap long-term borrowing |

| Rising interest rates | Increases cost of variable debt and limits appetite for new borrowing commitments |

| High inflation | Compresses margins and raises input costs, reducing capacity for debt service |

| Credit market tightening | Restricts access to new borrowing and raises the cost of refinancing existing debt |

| Bull equity market | Creates favorable conditions for equity issuance and convertible financing instruments |

| Recessionary environment | Pushes companies toward conservative financing and liquidity preservation strategies |

| Geopolitical instability | Raises risk premiums across financing markets, increasing borrowing costs for all |

| Loose monetary policy | Expands credit availability and supports both debt and equity market financing conditions |

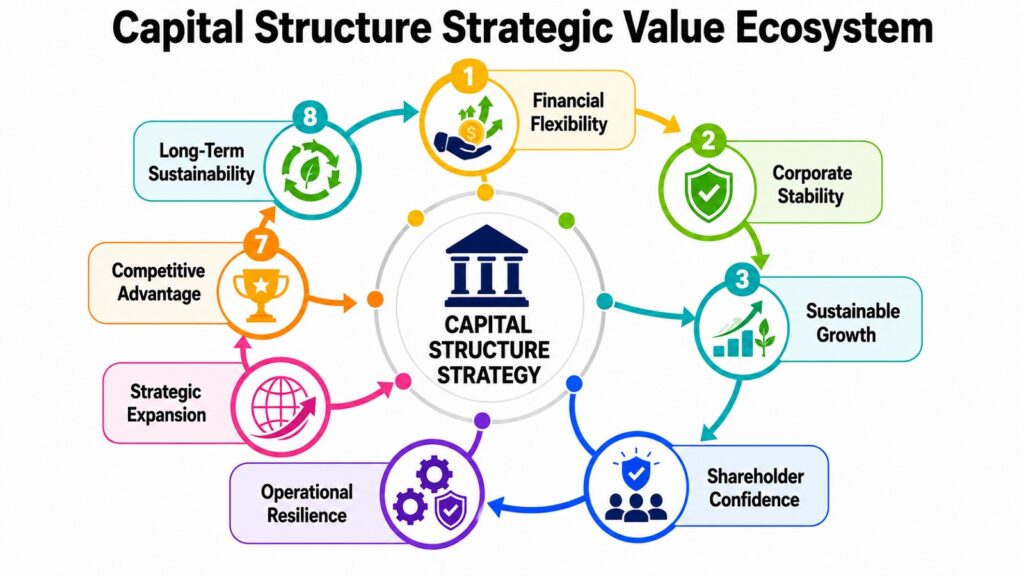

Conclusion: The Strategic Importance of Capital Structure

After exploring eight distinct pillars, one conclusion stands out clearly. Capital structure is not a background financial detail. It is a strategic framework that determines how a corporation competes, grows, survives difficulty, and ultimately creates value over time. The companies that manage their capital structure well are not simply following financial rules. They are making choices that shape every meaningful dimension of their long-term performance.

The eight pillars explored in this article each reveal a different way that financing decisions ripple through a business. Debt versus equity choices set the foundational risk and ownership profile. Cost of capital optimization determines how efficiently a company funds its operations. Financial risk management separates businesses that absorb shocks from those that collapse under pressure. Growth financing connects strategic ambition with funded execution. Shareholder value creation links financing discipline with investor confidence. Liquidity stability protects operational continuity. Lifecycle adaptation shows that no single financing approach works across all stages. And market condition sensitivity reminds us that capital structure must respond to external realities.

What unites these pillars is the recognition that capital structure requires active management rather than passive maintenance. Markets change. Business models evolve. Interest rates shift. Companies that revisit their financing strategies regularly, maintain honest assessments of their leverage, and preserve flexibility where it matters will consistently outperform those who treat capital structure as a set-and-forget policy.

For investors, understanding capital structure provides one of the clearest windows into the true financial health of any business. For leaders, managing it well is one of the most consequential responsibilities they carry.

Capital Structure: Strategic Importance of the 8 Pillars

| Pillar | Long-Term Relevance to Capital Structure |

| Debt vs Equity Financing | Defines the foundational risk profile and ownership dynamics of the corporation |

| Cost of Capital Optimization | Sustains competitive financing efficiency and maximizes long-term value creation |

| Financial Risk Management | Preserves solvency and operational flexibility through economic disruption cycles |

| Corporate Growth Financing | Enables sustained expansion without sacrificing financial stability or investor trust |

| Shareholder Value Creation | Aligns financing strategy with long-term investor expectations and return performance |

| Liquidity Stability | Ensures operational continuity and crisis resilience through disciplined cash management |

| Business Lifecycle Adaptation | Allows financing strategy to evolve alongside changing business needs and market access |

| Market Conditions Response | Keeps capital structure relevant and cost-efficient across shifting economic environments |