Table of Contents

Introduction: Corporate Governance As The Foundation of Modern Business

Corporate governance is an important aspect of modern businesses because it shapes nearly everything that matters inside an organization. It determines how decisions get made, who holds authority, how accountability is enforced, and whether long-term value actually gets created. Without governance, even well-intentioned businesses drift. With it, organizations develop the discipline to grow consistently and responsibly.

Many people still associate corporate governance with legal checklists and boardroom formalities. That picture is incomplete. Corporate Governance today has become an integral part of the business ecosystem. It works more like an operating system and runs quietly beneath leadership decisions, organizational culture, financial discipline, and stakeholder relationships. When governance is strong, those systems work in harmony. When it is weak, problems tend to surface in costly and visible ways.

The modern governance framework is no longer confined to a company’s upper floors. It reaches into how managers communicate expectations, how technology is deployed, how risks are identified before they escalate, and how organizations respond when things go wrong. Governance connects structure, culture, oversight, transparency, technology, strategy, and sustainability into one functioning whole.

This article is built around eight areas that together define what effective corporate governance looks like in practice. Each area addresses a distinct dimension of governance, yet none of them operates independently. Structure without ethics becomes rigid. Compliance without transparency becomes performative. Strategy without oversight becomes reckless. The real power of governance comes from how these areas reinforce each other.

Whether you are a business leader, a governance professional, or someone trying to understand how well-run organizations actually function, mastering these eight areas gives you a complete and practical view of corporate governance. The table below maps each area to its governance contribution and sets the foundation for what follows.

Table 1: Corporate Governance Framework — Eight Areas and Their Governance Contribution

| Corporate Governance Area | Corporate Governance Contribution |

| Governance Structure and Board Effectiveness | Defines authority, accountability, and oversight mechanisms across the organization |

| Corporate Ethics and Organizational Culture | Shapes behavioral norms and ensures governance values guide daily decisions |

| Risk Management and Internal Control | Identifies, monitors, and mitigates risks while strengthening decision reliability |

| Regulatory Compliance and Legal Governance | Establishes lawful operating frameworks and sustains organizational legitimacy |

| Transparency, Reporting, and Disclosure | Builds stakeholder trust through accurate, timely, and accessible information |

| Digital Governance and Technology Oversight | Aligns technology use with accountability, data integrity, and digital risk management |

| Strategic Oversight and Long-Term Value Creation | Connects governance decisions to sustainable performance and organizational resilience |

| ESG and Sustainable Governance | Integrates environmental, social, and governance factors into long-term business strategy |

1. Corporate Governance Through Governance Structure and Board Effectiveness

Corporate governance begins with structure because structure is what turns intentions into outcomes. Without clearly defined authority, responsibilities, and oversight routines, even well-designed governance principles remain theoretical. Governance structure is the architecture that decides who makes which decisions, who reviews those decisions, and what accountability looks like when outcomes fall short.

At the center of most governance structures sits the board of directors. But describing boards by their composition alone misses how governance actually works. What matters operationally is whether the board maintains genuine independence from management, whether directors bring the right mix of experience and judgment, and whether oversight functions happen with enough regularity and depth to catch real problems. A board that meets quarterly and reviews prepared summaries is structurally present but may not be functionally effective.

Governance effectiveness depends on mechanisms that operate beneath the board level as well. Committee structures allow specialized oversight of audit, risk, compensation, and nominations. Decision rights frameworks clarify which levels of the organization can commit resources, approve strategies, or enter contracts without escalation. Performance review cycles hold leadership accountable to defined objectives rather than to informal expectations.

What separates well-governed organizations from poorly governed ones is often not the presence of these mechanisms but the quality of how they operate. Governance structures work best when they balance control with operational agility. Excessive approval layers slow organizations down without improving decisions. Loose oversight creates room for misalignment and misconduct to grow undetected.

Leadership alignment also plays a defining role. When the board and executive leadership share a clear understanding of governance priorities, strategic intent, and risk appetite, governance works smoothly. When those two groups operate with different assumptions, governance gaps emerge. Effective governance structures make that alignment visible and routine rather than leaving it to goodwill.

Organizations that invest in strong governance structures build resilience into their foundations. They recover from disruption faster, adapt to change with less internal confusion, and demonstrate the kind of accountability that builds long-term credibility. Structure may not be visible to the outside world, but its effects always are. This structural discipline also sets the behavioral tone explored in the next section.

Table 2: Corporate Governance — Governance Structure Practices and Their Governance Role

| Corporate Governance Practices | Role in Corporate Governance |

| Board Independence | Prevents conflicts of interest and strengthens objective oversight |

| Audit Committee | Reviews financial reporting, internal controls, and external audit quality |

| Risk Committee | Oversees enterprise risk appetite and monitors exposure across the organization |

| Decision Rights Framework | Clarifies authority levels for resource commitment and strategic approvals |

| Performance Review Cycles | Holds leadership accountable to measurable organizational objectives |

| Board Evaluation Process | Assesses director effectiveness and identifies governance capability gaps |

| Succession Planning Oversight | Ensures leadership continuity and governance readiness for senior transitions |

| Governance Charter | Documents board responsibilities, authority limits, and operating procedures |

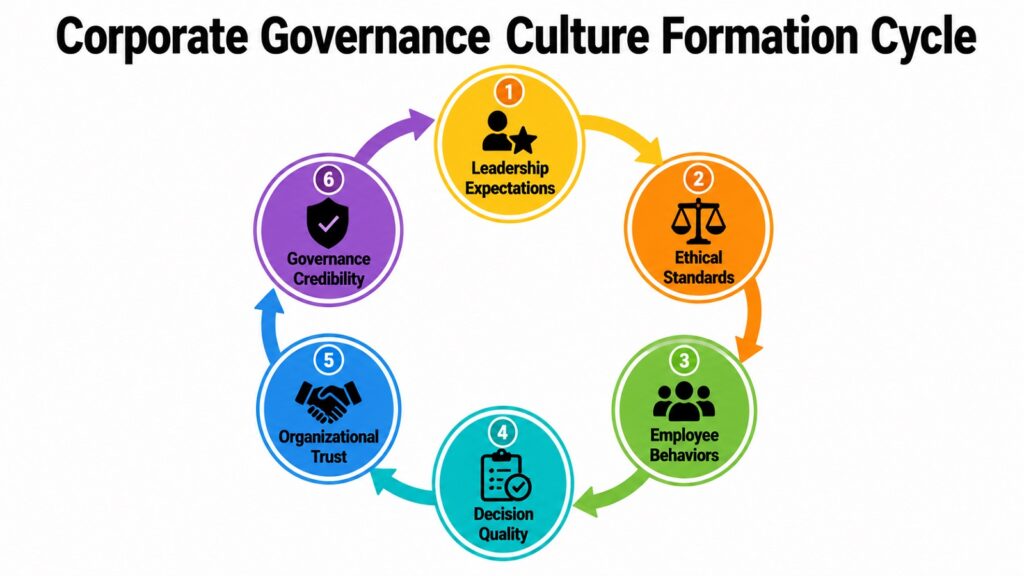

2. Corporate Governance Through Corporate Ethics and Organizational Culture

Corporate governance becomes effective only when formal systems are reinforced by the way people actually behave. Governance policies can be written with precision, but they only deliver results when the people inside the organization treat those policies as genuine expectations rather than compliance exercises. This is where ethics and organizational culture come in.

Culture is the execution layer of corporate governance. It determines how employees make decisions when no one is watching, how managers handle conflicts of interest, and how leaders respond when doing the right thing is inconvenient. Organizations with strong governance cultures do not rely entirely on rules to produce ethical behavior. They build environments where ethical decision-making becomes instinctive.

Tone at the top has real and measurable effects on governance quality. When senior leaders demonstrate consistent ethical behavior, take accountability seriously, and reinforce governance values through their own actions, those behaviors ripple through the organization. When leaders signal that results matter more than how results are achieved, ethical standards erode quickly, regardless of what the policy documents say.

Behavioral norms, accountability mechanisms, and governance values need to be communicated clearly and repeatedly. Organizations that treat ethics as a one-time training event miss the point. Governance culture is shaped by ongoing reinforcement, by how misconduct is handled, by how whistleblowers are treated, and by whether stated values align with actual decisions. Consistency between words and actions builds governance credibility.

Practical governance thinking in this area focuses on designing systems that make ethical behavior easier and misconduct harder. This includes reporting channels that actually get used, performance frameworks that reward governance discipline alongside financial outcomes, and leadership development programs that treat ethical judgment as a core capability. Ethics also supports decision quality by reducing the uncertainty and conflict that arise when behavioral expectations are unclear.

Culture alone, however, cannot sustain governance without disciplined monitoring and controls. Organizations need structured oversight to verify that ethical standards are being met and to catch exceptions before they become patterns. The connection between culture and control is essential to governance durability.

Table 3: Corporate Governance — Ethics and Culture Indicators in Governance Practice

| Ethics and Culture Indicator | Corporate Governance Significance |

| Tone at the Top | Leadership behavior sets the ethical standard across all organizational levels |

| Code of Conduct | Defines acceptable behavior and establishes clear ethical boundaries |

| Whistleblower Protection | Encourages reporting of misconduct without fear of retaliation |

| Conflict of Interest Policy | Manages situations where personal and organizational interests diverge |

| Ethics Training Programs | Builds consistent understanding of governance values across the workforce |

| Accountability Mechanisms | Ensures consequences are applied consistently when governance standards are breached |

| Behavioral Performance Metrics | Measures ethical conduct alongside financial results in leadership reviews |

| Speak-Up Culture | Creates psychological safety for raising governance concerns internally |

3. Corporate Governance Through Risk Management and Internal Control

Corporate governance is only as strong as its ability to protect the organization from uncertainty. Risk management and internal control are the mechanisms that transform governance from aspiration into operational resilience. When organizations can see their risks clearly and respond to them with discipline, governance becomes a genuine source of strategic confidence.

Risk management in the governance context is about visibility and response. Organizations face a wide range of risks: operational failures, financial misstatements, strategic miscalculations, regulatory breaches, reputational damage, and increasingly, risks that emerge from digital systems and global disruptions. Effective governance requires that these risks are identified systematically, prioritized by potential impact, assigned clear ownership, and monitored on a regular basis.

The internal control environment enhances governance by fostering accountability across the organization. Controls are not simply procedural checkpoints; they are crafted to guarantee that decisions made at all levels of the organization are dependable, authorized, and aligned with established objectives. When internal controls are effectively designed and properly upheld, the organization benefits from a systematic framework that verifies whether intended outcomes are indeed being realized.

Risk governance also involves setting an explicit risk appetite. Organizations need to define how much uncertainty they are willing to accept in pursuit of their strategic goals. This is a governance decision, not a technical one. A board that has not discussed risk appetite with management has left a critical governance gap. When risk appetite is defined and communicated, managers at every level can make faster and more confident decisions within known boundaries.

The relationship between risk awareness and business outcomes is direct. Organizations that detect emerging risks early have more options for response. Those that discover risks late face compressed timelines, limited choices, and greater potential damage. Internal audit functions, control self-assessments, and risk reporting routines all exist to give governance systems earlier visibility into where problems are developing.

Strong risk management also builds confidence among investors, lenders, regulators, and other stakeholders. When organizations demonstrate that they have structured approaches to identifying and managing uncertainty, external parties have greater reason to trust the organization’s governance. This controlled environment also connects naturally to the need for formal compliance structures.

Table 4: Corporate Governance — Risk Categories and Internal Control Practices

| Risk Category / Control Practice | Corporate Governance Function |

| Operational Risk Management | Identifies and reduces risks from process failures, human error, and system breakdowns |

| Financial Risk Controls | Ensures accuracy and reliability of financial reporting and asset management |

| Strategic Risk Oversight | Monitors risks arising from business model changes and competitive shifts |

| Risk Appetite Statement | Defines acceptable risk thresholds aligned with organizational strategy |

| Internal Audit Function | Provides independent assurance on the effectiveness of governance and controls |

| Control Self-Assessment | Enables business units to evaluate their own governance and control environment |

| Incident Reporting System | Captures and escalates control failures for timely governance response |

| Emerging Risk Monitoring | Identifies new threats from regulatory, digital, and macroeconomic developments |

4. Corporate Governance Through Regulatory Compliance and Legal Governance

Corporate governance depends on organizations operating within lawful and disciplined frameworks, but compliance should never be mistaken for the end goal. Treating compliance as the ceiling of governance ambition leads to organizations that follow rules minimally and miss the deeper value that governance can deliver. The right framing positions compliance as an enabler of confidence in corporate governance rather than a constraint on business activity.

Legal governance involves establishing the policies, accountability standards, and monitoring routines that keep an organization aligned with applicable laws, regulations, and governance codes. This includes corporate law requirements, securities regulations, data protection frameworks, environmental obligations, labor standards, and sector-specific rules. Organizations operating across multiple jurisdictions face the additional challenge of managing diverse and sometimes conflicting legal expectations.

Governance systems create compliance consistency by embedding legal awareness into operational routines rather than treating it as a periodic review exercise. Compliance officers, legal teams, and board-level oversight all play roles in this process, but effective compliance governance requires that business managers also understand their own accountability within the framework. When compliance is owned only by specialists, it tends to operate at the edges of the business rather than at the center.

The governance discipline around compliance also includes adapting to changing expectations. Regulations evolve. Legal interpretations shift. Industry standards get updated. Organizations with mature governance frameworks build in mechanisms to monitor these changes, assess their implications, and update internal practices accordingly. Those that wait for enforcement action to discover compliance gaps pay a significantly higher price.

Compliance governance builds organizational legitimacy. When stakeholders, including investors, regulators, customers, and communities, observe that an organization operates with legal integrity and governance discipline, trust increases. That trust translates into practical advantages: easier access to capital, smoother regulatory relationships, stronger partnerships, and greater resilience during periods of scrutiny.

Compliance becomes most effective when it is supported by transparency and open internal reporting. The connection between these two dimensions of governance becomes the focus of the next section.

Table 5: Corporate Governance — Compliance Standards and Legal Governance Mechanisms

| Compliance Area / Corporate Governance Mechanism | Corporate Governance Role |

| Corporate Law Compliance | Ensures adherence to foundational legal obligations governing the organization |

| Securities Regulation | Governs disclosure and trading conduct for publicly listed companies |

| Data Protection Framework | Manages legal obligations around personal data handling and privacy |

| Anti-Corruption Governance | Establishes controls to prevent bribery, fraud, and improper conduct |

| Regulatory Monitoring Process | Tracks changes in applicable laws and updates internal governance practices |

| Compliance Accountability Structure | Assigns clear responsibility for legal governance at each organizational level |

| Policy Review Cycle | Ensures governance policies remain current and reflect legal expectations |

| Regulatory Engagement | Maintains constructive relationships with oversight bodies and regulators |

5. Corporate Governance Through Transparency, Reporting, and Disclosure

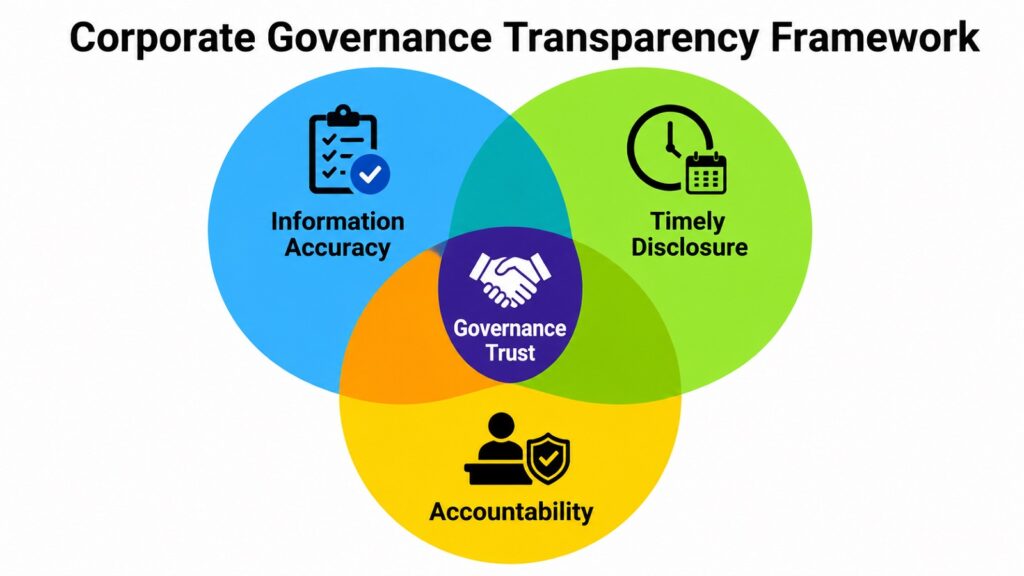

Corporate governance creates trust when the people making decisions can be seen, and when the information they rely on is available to those affected by the outcomes. Transparency is not simply an obligation to publish reports. It is an active governance capability that shapes how stakeholders understand an organization, how internal decisions get made, and how accountability is exercised when performance falls short.

Reporting serves as one of the primary tools through which governance becomes visible. Financial statements, annual reports, risk disclosures, governance statements, and sustainability reports all give different stakeholders insight into the health and direction of the organization. But the quality of these reports matters as much as their existence. Governance reporting that is delayed, incomplete, or difficult to interpret weakens rather than strengthens the trust it is designed to build.

The quality of disclosure serves as a quantifiable indicator of governance. Organizations that provide clear and consistent disclosures indicate transparency, showing they have nothing to conceal and that they value stakeholders’ capacity to make informed decisions. Selective disclosure, which emphasizes positive developments while downplaying risks, results in short-term impression management that undermines long-term credibility. Regulators and discerning investors have become increasingly adept at identifying this behavior, and the governance repercussions of such discoveries are substantial.

Internal transparency is equally important to external disclosure. When information flows freely within the organization, management can make decisions with better data, board members can exercise oversight with greater clarity, and employees can align their work with strategic priorities. Information silos reduce governance effectiveness by creating blind spots at every level of the organization. Governance frameworks that prioritize internal transparency tend to make faster and better-calibrated decisions.

Communication discipline also matters. Governance reporting should be structured to serve the needs of its audience, whether that audience is the board, investors, regulators, employees, or the public. Information that is technically accurate but poorly structured for its audience fails the governance purpose it is meant to serve.

Transparency also reduces uncertainty among stakeholders. When organizations communicate consistently about strategy, risk, and performance, external parties are less likely to fill information gaps with speculation. Governance credibility depends significantly on this reduction of uncertainty, and it connects directly to the governance challenges that digital systems now present.

Table 6: Corporate Governance — Transparency and Disclosure Practices

| Disclosure Practice / Transparency Indicator | Corporate Governance Contribution |

| Annual Report and Accounts | Provides a comprehensive financial and governance overview to stakeholders |

| Board Governance Statement | Communicates how governance structures and responsibilities are organized |

| Risk Disclosure | Informs stakeholders of material risks and how they are being managed |

| Related-Party Transaction Disclosure | Ensures transparency around potential conflicts of interest at senior levels |

| Sustainability and ESG Reporting | Shares progress on environmental, social, and governance commitments |

| Timely Financial Reporting | Demonstrates governance discipline through consistent and punctual disclosure |

| Internal Reporting Systems | Ensures relevant information reaches decision-makers at the right time |

| Stakeholder Communication Policy | Establishes consistent standards for how information is shared externally |

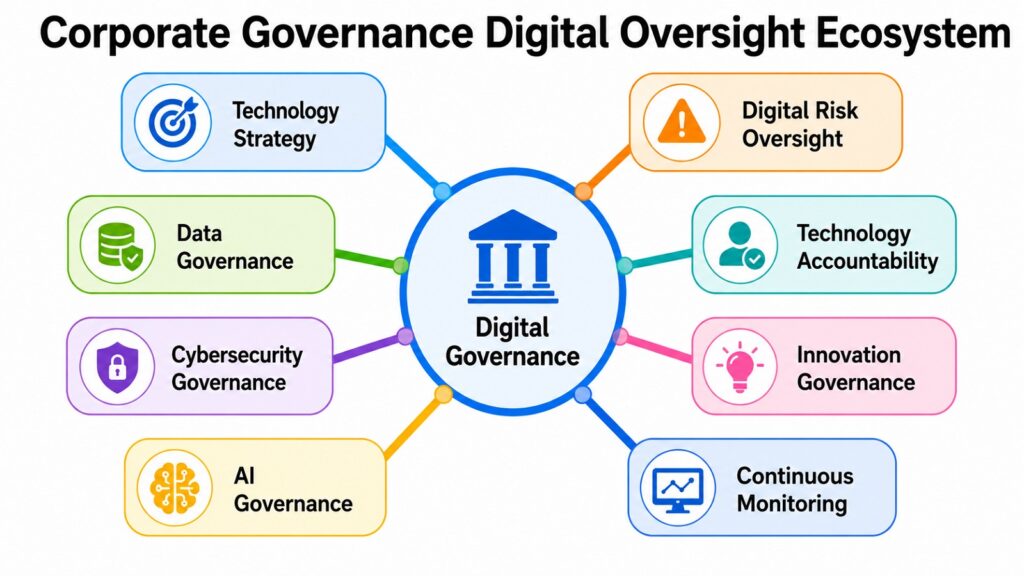

6. Corporate Governance Through Digital Governance and Technology Oversight

Corporate governance increasingly depends on governing technology rather than merely using it. As digital systems become core to how organizations operate, compete, and communicate, technology oversight has moved from an IT function into a central governance responsibility. Organizations that treat digital governance as an afterthought carry structural risks that boards and leadership teams can no longer afford to ignore.

Digital governance is the set of policies, accountabilities, and oversight mechanisms that ensure technology serves the organization’s goals without introducing unmanaged risk. This includes decisions about how data is collected, stored, used, and protected. It includes the governance frameworks around cybersecurity, which is no longer a purely technical concern. A significant data breach or ransomware incident is a governance failure as much as a technology failure, and boards are increasingly expected to own that accountability.

Oversight of technology also encompasses the responsible management of artificial intelligence. As AI systems are utilized for decision-making, customer engagement, risk evaluation, and operational automation, governance frameworks must tackle issues related to transparency, bias, accountability, and explainability. The European Union’s AI Act, which took effect in 2024, marks a significant regulatory advancement that mandates organizations to categorize AI systems based on their risk levels and implement governance standards accordingly.

Data governance is another dimension that sits at the intersection of digital oversight and corporate governance. Organizations hold increasing volumes of sensitive data about customers, employees, and partners. The governance obligation is to ensure that this data is handled with integrity, that access is controlled appropriately, and that data quality is maintained to support reliable decision-making. Poor data governance creates both regulatory exposure and operational risk.

Digital risk introduces new categories of uncertainty that governance frameworks must address. These include third-party technology dependencies, vendor concentration risk, digital infrastructure vulnerabilities, and the governance implications of cloud migration. Board-level digital literacy has become a governance capability requirement rather than a desirable characteristic. Organizations whose boards lack the capacity to understand and challenge digital strategy carry governance gaps that compound over time.

Digital governance, done well, aligns innovation with accountability. It enables organizations to pursue technological advantage while maintaining the discipline and oversight that governance requires. That disciplined approach to technology also sets the conditions for the strategic governance explored in the next section.

Table 7: Corporate Governance — Digital Governance Practices and Technology Oversight Concepts

| Digital Governance Practice | Governance Significance |

| Cybersecurity Governance Framework | Establishes board-level accountability for digital risk and incident response |

| Data Governance Policy | Defines standards for data quality, access control, and responsible data use |

| AI Governance Framework | Ensures AI systems are deployed with transparency, fairness, and accountability |

| Third-Party Technology Risk | Manages governance obligations arising from vendor and cloud dependencies |

| Digital Risk Oversight | Integrates emerging technology risks into enterprise risk governance |

| Board Digital Literacy | Builds governance capacity to challenge and direct digital strategy |

| Incident Response Governance | Defines escalation, communication, and accountability protocols during digital events |

| Technology Investment Oversight | Ensures technology spending aligns with strategic governance priorities |

7. Corporate Governance Through Strategic Oversight and Long-Term Value Creation

Corporate governance reaches its most meaningful expression when it actively shapes strategy rather than simply reviewing it. Many governance frameworks operate in a reactive mode, approving proposals that management brings forward and monitoring compliance with existing plans. Mature governance takes a more engaged posture, contributing to the quality of strategic thinking and holding leadership accountable for the logic and sustainability of their strategic choices.

Strategic oversight in the governance context means the board and leadership team work with a shared and current understanding of the organization’s competitive position, long-term value drivers, and material risks. This is not micromanagement. It is the governance discipline that ensures major decisions are scrutinized from multiple perspectives before they are committed to. Capital allocation decisions, acquisition strategies, market entry choices, and major transformation programs all carry governance implications that extend well beyond financial modeling.

Performance governance connects strategic ambition to real accountability. Organizations that set clear strategic objectives and then measure progress with transparency create governance conditions where underperformance becomes visible before it becomes entrenched. Key performance indicators, milestone reviews, and strategic progress reporting all serve governance functions when they are designed honestly and used consistently rather than selectively.

Resource allocation is a governance question as much as a management question. How organizations invest their capital, talent, and attention reveals their true priorities far more accurately than their stated strategies. Governance oversight of resource allocation ensures that investment decisions align with long-term value creation rather than short-term visibility. This becomes especially important when external pressures push for immediate financial results at the expense of longer-term organizational health.

The direction of innovation is also included in the realm of strategic governance. Organizations that effectively manage innovation establish frameworks that differentiate between exploratory investments, which may require years to yield returns, and the core business activities that ensure short-term performance. Boards that recognize this distinction can safeguard innovation investments during times of financial strain rather than eliminating them as a straightforward cost-cutting measure.

The OECD Principles of Corporate Governance, updated in 2023, emphasize that boards should actively engage in strategy oversight and the creation of long-term value. Governance that aligns decisions with sustainable outcomes fosters organizational resilience and builds stakeholder trust. This forward-looking approach becomes increasingly vital when sustainability factors are integrated into the governance framework.

Table 8: Corporate Governance — Strategic Governance Practices and Long-Term Value Drivers

| Strategic Corporate Governance Practice | Long-Term Corporate Governance Contribution |

| Strategic Plan Oversight | Ensures the board reviews and challenges the long-term direction of the organization |

| Capital Allocation Governance | Aligns investment decisions with sustainable value creation priorities |

| Performance Governance Framework | Connects strategic objectives to measurable accountability mechanisms |

| Innovation Investment Oversight | Protects exploratory investment during periods of short-term financial pressure |

| Mergers and Acquisitions Governance | Applies structured oversight to major transactions and their strategic rationale |

| Succession and Leadership Pipeline | Ensures long-term organizational capability through planned leadership development |

| Stakeholder Value Alignment | Balances the interests of shareholders, employees, customers, and communities |

| Strategic Risk Integration | Connects risk management directly to strategic planning and governance review |

8. Corporate Governance Through ESG and Sustainable Governance

Corporate governance has expanded significantly over the past decade to incorporate environmental, social, and governance considerations as core elements of long-term oversight. This is not a departure from traditional governance thinking. It is an evolution of it. Boards and organizations that treat ESG as a separate program sitting alongside governance have missed the more important insight: sustainability is increasingly a governance matter, not simply a reputational one.

Environmental governance involves accountability for how organizations manage their impact on natural systems, manage resource consumption, and respond to climate-related risk. The Task Force on Climate-related Financial Disclosures framework, now embedded into the regulatory requirements of multiple jurisdictions, including the United Kingdom and Australia, requires organizations to assess and disclose how climate risk affects their strategy, governance, and financial outlook. This is a governance obligation, not a marketing exercise.

Social governance covers how organizations manage their relationships with employees, supply chains, communities, and broader society. This includes labor standards, human rights due diligence, workplace safety, diversity and inclusion practices, and community impact. Governance frameworks that address social dimensions recognize that organizational legitimacy depends on the quality of these relationships over time. Ignoring social governance creates risks that range from workforce disengagement to regulatory scrutiny to reputational damage.

The governance aspect of ESG pertains to the caliber of decision-making frameworks, accountability systems, and ethical principles examined in this article. ESG frameworks enhance traditional governance by establishing a clear expectation that these structures must integrate long-term and systemic viewpoints, rather than solely concentrating on short-term financial outcomes.

Integrated ESG governance requires that sustainability considerations are embedded into board responsibilities, executive performance incentives, risk management frameworks, and capital allocation decisions. This is increasingly the expectation of institutional investors. Major asset managers, including BlackRock and Vanguard, have consistently communicated governance expectations around ESG integration in their annual stewardship statements over recent years.

Sustainable governance also prepares organizations for the regulatory direction of travel. ESG disclosure requirements are expanding across major markets, including the European Union’s Corporate Sustainability Reporting Directive (CSRD), which requires large companies to report on sustainability alongside financial performance. Organizations that build sustainable governance practices now are better positioned for these requirements and for the investor scrutiny that accompanies them.

Table 9: Corporate Governance — ESG Dimensions and Sustainable Governance Practices

| ESG Dimension / Corporate Governance Practice | Corporate Governance Significance |

| Climate Risk Governance | Integrates climate-related financial risks into board oversight and strategy |

| Environmental Impact Accountability | Assigns governance responsibility for managing resource use and ecological impact |

| Human Rights Due Diligence | Ensures supply chain and operational practices meet social governance standards |

| Workforce Governance | Manages labor standards, safety, and employee welfare as governance obligations |

| ESG Reporting Framework | Provides structured disclosure of sustainability performance to stakeholders |

| Sustainability in Executive Incentives | Links leadership compensation to measurable ESG and governance outcomes |

| Diversity Governance | Embeds inclusive decision-making and representation into governance structures |

| Long-Term Value Accountability | Holds boards responsible for balancing financial returns with broader societal impact |

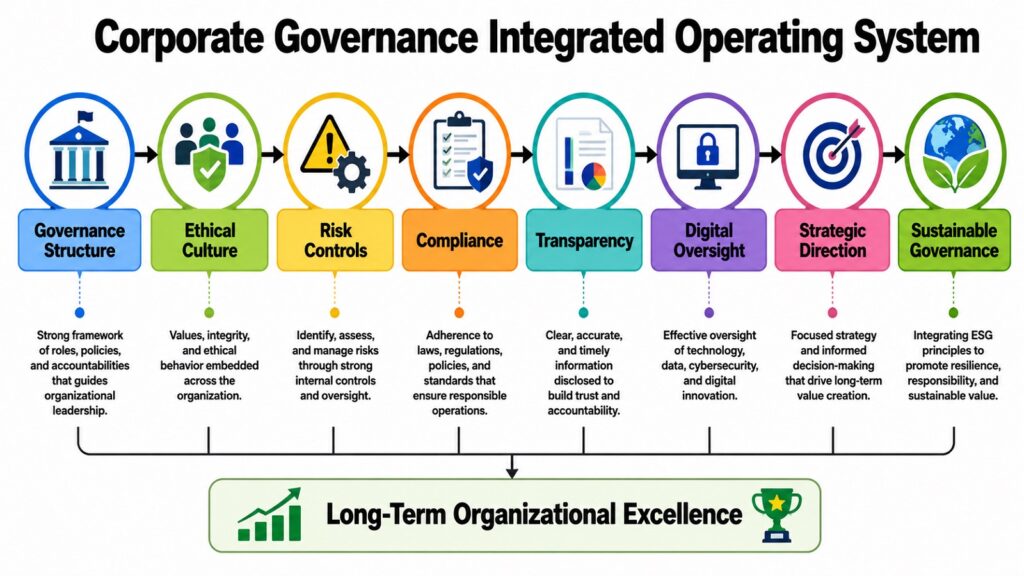

Conclusion: Corporate Governance for Long-Term Business Excellence

Corporate governance is not a collection of separate obligations. It is a connected system where each area reinforces the others. Structure creates the architecture for accountability. Ethics and culture give that structure meaning. Risk management and compliance protect the organization from the hazards that governance is designed to anticipate. Transparency builds the trust that allows governance to function with external credibility. Digital governance extends accountability into the technologies that now run modern business. Strategic oversight ties governance to long-term performance. And ESG governance ensures that the organization’s obligations extend beyond its own financial interests.

Governance quality is not determined by how many policies an organization has written. It is determined by how consistently those policies are reflected in actual decisions, behaviors, and outcomes. Organizations that treat governance as a living capability rather than a compliance artifact tend to make better decisions, recover from setbacks more effectively, and build deeper relationships with the stakeholders who matter most to their long-term success.

The eight areas covered in this article collectively represent a complete governance framework. Each area is also a domain of governance practice rich enough to warrant its own deeper exploration. Future articles in this series will examine each area in more detail, providing the tools, frameworks, and analysis needed to strengthen governance in practice.

Organizations that invest seriously in corporate governance create a competitive advantage that is difficult to replicate quickly. Governance takes time to build and requires consistent leadership commitment to maintain. But the returns, measured in organizational resilience, stakeholder confidence, and long-term value, make that investment worthwhile.

Table 10: Corporate Governance — Eight Areas and Their Primary Governance Outcome

| Governance Area | Primary Corporate Governance Outcome |

| Governance Structure and Board Effectiveness | Accountable authority and disciplined organizational oversight |

| Corporate Ethics and Organizational Culture | Ethical behavior embedded in daily decisions and governance conduct |

| Risk Management and Internal Control | Protected continuity and reliable decision-making under uncertainty |

| Regulatory Compliance and Legal Governance | Legal integrity and sustained organizational legitimacy |

| Transparency, Reporting, and Disclosure | Informed stakeholders and strengthened governance credibility |

| Digital Governance and Technology Oversight | Accountable technology use and managed digital risk |

| Strategic Oversight and Long-Term Value Creation | Aligned strategy and durable organizational performance |

| ESG and Sustainable Governance | Responsible governance that supports long-term business resilience |